-

BackWhat we doNumis is an ambitious, dynamic and innovative investment bank, driven to excel across all aspects of its delivery.Investment Banking

-

BackLatest newsRead the latest news about our business, our people and our work, find out about our next events and conferences.News

-

BackWho we areOur collaborative environment and distinctive way of excelling , is nothing without our great people.

-

BackOur board

Numis at a glance

Our Articles

28

Mar 2024

31

Jan 2024

Latest Transactions

London Stock Exchange Group PLC

£1.4bn

Co-global coordinator on the £1.4 billion sell-down of the London Stock Exchange Group PLC

March 2024

Custodian Property Income REIT

£237m

Sole financial adviser, sponsor and corporate broker

January 2024

Numis On Twitter

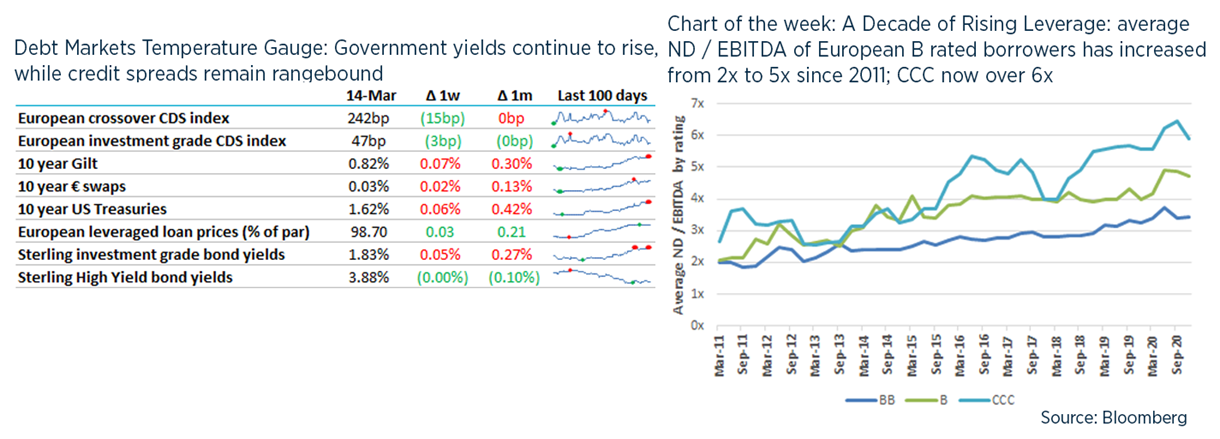

Debt Advisory Update

On the anniversary that the pandemic was declared by the WHO, the ONS changed its inflation basket this week. In: hand sanitiser, men’s jogging bottoms and dumbbells. Out: work canteen sandwiches, ground coffee and white chocolate.

TL / DR: Further Greensill Fallout; Limits on Leverage; Virgin Active Workout Cramdown

A bit more Greensill

- Following last week’s Greensill news, some potential losers / bagholders have emerged:

- Several German towns look like losing €600m of deposits with Greensill Bank AG (which until its troubles last week was rated BBB+ by Scope). Seems they forgot the lesson of the UK councils depositing at the Icelandic banks in 2008 (I hadn’t realised that the councils had typically recovered 90-100%, after 6 years).

- Scope should take some professional pride that its ratings report here correctly identified what ultimately wrong: weak governance, loss of insurance cover, delayed or sub-par recoveries, and loss of reputation.

- Thousands of Australian and UK steel workers who face redundancy unless someone takes on their plants (but not Rio Tinto, Tata and ArcelorMittal which sold them all to GFG) and the UK and Scottish Governments which together seemed to have guaranteed almost £1bn of Gupta loans.

- Reinsurers: Tokio Marine and the insurer IAG both claim to have ‘zero net exposure’ to Greensill on credit insurance policies for the benefit of Greensill’s investors. This is partly because they don’t believe they are on the hook in the first place and / or because they have obtained reinsurance.

- Credit Suisse: CS may not get much for its $140m holdco pre-IPO loan to Greensill and it may also feel the need to step up for its investors to alleviate reputational damage.

Limiting Private Equity Leverage

- “Deal by deal” for a private equity investor can generate better and earlier expected returns for the General Partner (PE shop) than a big blind fund: bad deals don’t contaminate fees / carried interest due from good deals. Some institutional LPs like deal-by-deal because they are taking less on trust as they can evaluate deals in advance. (It can make executing deals harder, particularly for auctions).

- This mirrors more a more fundamental point about PE structures: keeping things in silos can increase equity value. Take a PE portfolio of 5 businesses each financed standalone: high leverage combined with limited liability for shareholders means that one problem child may not have much impact on overall fund returns. Contrast with this a conglomerate owning these business with lower leverage cross-collateralised across all the divisions. The diversification may reduce its debt costs but its equity holders don’t benefit from the volatility across each asset. See also a basket of options is worth more than an option on a basket.

- Prompted by high profile failures such as Toys R Us, some US and European policymakers have long considered at how to curb PE sponsors and their financial leverage, particularly when it comes to impact on wider stakeholders such as pensioners or employees.

- Some mooted restrictions include:

- Remove tax deductibility of interest (which favours debt over equity): discussed for decades and likely only through OECD coordination, given tax competition, just like the BEPS project. Thin Capitalisation rules have an impact but they typically don’t stop PE companies getting interest cost deductions. More discussion here.

- Remove limited liability for portfolio companies: “piercing the corporate veil” is unusual: UK pension rules can penetrate the corporate veil, as can UK divorce courts. Elizabeth Warren proposed the neutrally-titled “Stop Wall Street Looting Act” in 2019 which would have made PE firms responsible for liabilities of their portfolio investments, including pensions. For good measure, she also threw in removing tax deductions for debt. This died in Republican committees in 2019 but could well be revived by a Democrat Senate & Presidency.

- Put more responsibility onto management: A new one to me, from a US legal case last year: the ex-management of Nine West were held by the NY District Court to be liable for breach of their fiduciary duties following the recommended buyout by Sycamore Group (PE) and the subsequent bankruptcy. It’s an unusual fact pattern (here) but the takeaway is “US directors recommending a cash offer have a duty to examine the solvency of the business after it has been sold”.

Virgin Active Workout Cramdown

- Live in the courts: Virgin Active using the UK’s new “Super Scheme” rules cramdown dissenting landlords; full announcement here.

- The novel part is using support from lenders to force landlords onside through a “cross class cramdown” – not a game of sardines but a means of stopping smaller classes of creditors from “holding up” restructurings. More about this here and here.

- This innovation may help the UK remain the European destination for corporate restructurings after Brexit as it turns out that the Withdrawal Agreement didn’t address this important practice (just like for the rest of UK financial services).

- Other European countries like the Netherlands have improved restructuring mechanics to take advantage of Brexit, enabling a court-ordered moratorium on enforcement, improbably called WHOA.

- Both of these measures are simply catching up with US Chapter 11, though in a couple of ways the Dutch code is now more flexible. It’s impressive that the US has maintained such an efficient bankruptcy system given the extensive availability of litigation – I think the ability to implement Debtor-In-Possession finance is a big part of this.

UK debt financings this week:

- WH Smith extended maturity on its two £200m term loans by one year (to Oct-23) alongside new minimum liquidity covenants.

- Busy Bees (nurseries) closed on a dual currency TLB tightening pricing by 25bp on the EUR tranche - £365.8m tranche to L + 4.75bp/99 OID/0% floor and the €257m tranche at E+375bp/99 OID/0% floor.

- EG Group finalised pricing on the USD portion of their upsized $510m financing to L+425bp/99 OID.

- Victoria plc was back in the market again with a €250m 3NC2 seven year high yield bond deal at 3.75%. Password for the roadshow was Meghan2021 …

- Heathrow priced a £350m 7-year Class B bond at G+215bp, despite passenger numbers being down by 84% for the second half of 2020 vs 2019 .

- Cadent (UK gas distributor) sold €625m of Transition Bonds at mid-swaps + 70bp – these “nearly green bonds” issued by corporates that cannot quite claim to be green yet. Interesting discussion here.

Our services

Numis is an ambitious, dynamic and innovative investment bank, driven to excel across all aspects of its delivery.