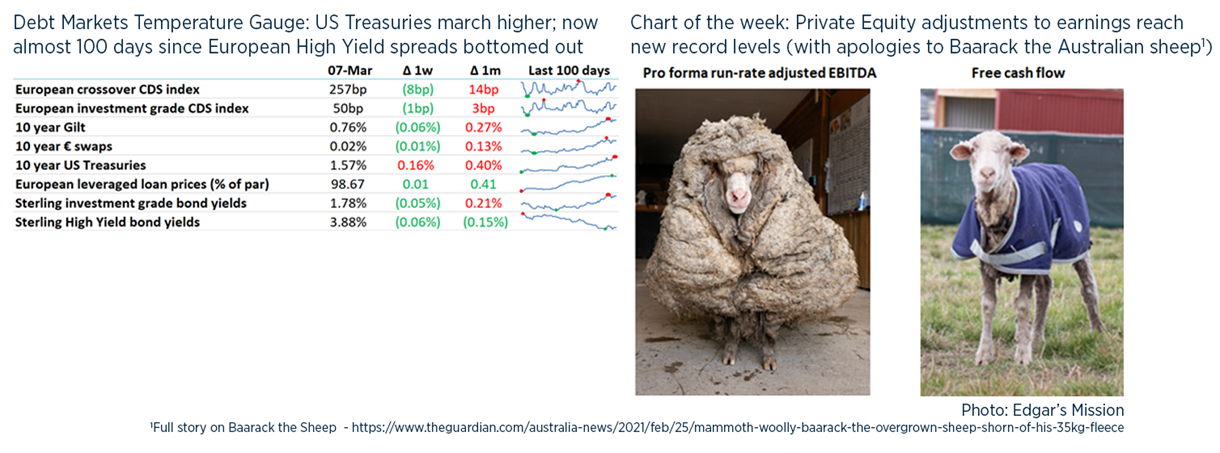

-

BackWhat we doNumis is an ambitious, dynamic and innovative investment bank, driven to excel across all aspects of its delivery.Investment Banking

-

BackLatest newsRead the latest news about our business, our people and our work, find out about our next events and conferences.News

-

BackWho we areOur collaborative environment and distinctive way of excelling , is nothing without our great people.

-

BackOur board

Numis at a glance

Our Articles

28

Mar 2024

31

Jan 2024

Latest Transactions

London Stock Exchange Group PLC

£1.4bn

Co-global coordinator on the £1.4 billion sell-down of the London Stock Exchange Group PLC

March 2024

Custodian Property Income REIT

£237m

Sole financial adviser, sponsor and corporate broker

January 2024

Numis On Twitter

Debt Advisory Update

Today marks the end (for now at least) of homeschooling, proof that teachers have more effective authority over children than their parents.

Something a little different this week: the Greensill / GFG story has been front page news of the FT for 5 days out of 6, and I’ve been fascinated by Greensill for years, so I thought I’d focus on this.

TL / DR: Greensill, Greensill, Greensill

1. What is Supply Chain Finance anyway?

- Short answer: “reverse factoring” where the payor organises the receivables financing rather than the payee.

- This FT article is a good explainer: small suppliers of a large corporate with good credit can get paid early on outstanding invoices by joining a programme where a bank buys the invoice at a small discount. Any single small supplier probably couldn’t finance as well against this receivable because of the set-up costs and small size of one receivable. But the programme efficiently aggregates lots of suppliers enabling faster payment at lower cost.

- There’s a lot of it about: this PwC report by the improbably-named Simon Templar (what were his parents thinking?) suggests that over 55% of businesses are using Supply Chain Finance.

- Supply Chain Finance was promoted by David Cameron’s government in 2012 as “an innovative way for large companies to help their supply chain access credit, improve cash-flow and at a much lower cost, and has already been successfully implemented by companies including Rolls Royce and Vodafone.” Vodafone and Cameron will come up again in this story …

- Santander was a pioneer of this financing in the 1980s, spurred on by high inflation and high interest rates. This was picked up by Fiat and then Carrefour and enabled improved operating margins: suppliers would agree to lower prices in return for being paid earlier by the banks, which were happy to take the customer’s credit at low credit margins.

- In passing, the rules of trade finance were first written down Hammurabi, the King of Babylonia in 1750BC: s106 and s107 deal with repudiated debts and their punishments. (s110 is pretty awful).

- Maybe an easier solution to getting cash to suppliers sooner could be the credit-worthy customer simply paying sooner (e.g. dynamic discounting).

- One reason for banks to get involved is price as shown in this table: if the going rate for being paid sooner by a good quality corporate is 1% per month then there is plenty of scope for a bank to intermediate but still get a great return on assets for a 30-60 day uncommitted exposure – imagine being paid L+185bp for a short-dated Nestle exposure!

- For me, the biggest problem with Supply Chain Finance is the increase in refinancing risks from becoming dependent on the credit decisions of 1 or 2 banks instead of a multitude of suppliers – in fact, any one of 5-10 individuals in that bank could probably veto the scheme. Moody’s and Fitch gave good write-ups of the problems a couple of years age.

2. So what was different about Greensill Capital?

- Mainly its founder Lex Greensill, who sounds like a James Bond villain and persuaded General Atlantic and SoftBank to invest c.$1.75bn, and who started life selling the raw materials for Bundaberg Rum and ended up with four private jets and a CBE from Prince Charles.

- SoftBank has apparently written down its $1.5bn investment to zero and the WSJ reported an unusual transaction where Greensill lent $350m back to General Atlantic.

- From a financial perspective, Greensill’s key innovation was to turbocharge complexity: using trade credit insurers to take some risk, his own bank to warehouse deals before launching to the capital markets and leveraging government support from the Scottish and UK governments. What was left over was sold to (it seems mainly) GAM and Credit Suisse customers. GAM has been badly damaged by its Greensill funds and Credit Suisse might have to step in to ensure investors in its $10bn fund don’t face losses – this reminds me of when WestLB had to guarantee $11bn of SIV deals in 2007.

- At least the UK government has found a way to cancel its CLBILS guarantee – maybe the Scottish government might hear back on this this £575m guarantee soon.

- Even more unusual still was Vodafone’s circular financing deal which saw it invest some of its free cash in a fund that was backed by receivables due to suppliers from Vodafone. In another circular aspect, Greensill hired Vodafone’s Treasurer to be its CFO – and David Cameron to be a Senior Adviser.

- There is more to go on this: Greensill Bank faces criminal prosecution in Germany, Apollo is picking over the operating business of Greensill, apparently willing to spend $100m on its software system, though it may re-trade this in the absence of any competing bids, and Greensill’s main Trade Credit Insurer is accusing one its own staff of exceeding delegated authority in approving $10bn of trade credit insurance.

3. What’s the wider impact?

- Most pressing, Greensill is no longer originating new Supply Chain Financing: any of its clients reliant on this is now facing a working capital crunch, with maybe 50,000 jobs at risk.

- Any business relying on Supply Chain Finance might need to wean themselves off this, as did Mitie a few years ago (incidentally Mitie’s analysis of “Total Financial Obligations” debt-like items is exceptional – see p11 here).

- Greensill’s main client GFG Alliance is a very opaque family-owned group of steel businesses controlled by Sajeev Gupta and which employs 35,000 globally and 5,000 in the UK. GFH has been very reliant on Greensill to fund its rapid expansion, with some estimates of almost £2bn being advanced by Greensill to GFG for acquisitions. In 2019, GFG struggled to sell $375m of high yield debt at 12% so replacing Greensill will be difficult – and Greensill recently solidified a pledge over GFG’s UK business. Anyone up for a challenge can apply for an internal audit job at GFG here.

- GFG / Gupta also owns a UK bank called Wyelands, which the Bank of England this week forced a £75m equity injection and required all retail depositors to be repaid, after reports the bank was largely financing GFG – this is an unprecedented move by the BoE.

- Other big clients of Greensill include Telstra, CIMIC, Bluestone Resources, Nokia, General Mills, Astra Zeneca, Newell, Henkel. Full details here.

- Plenty of accounting red flags: changing year end dates, imbalance between size of business and its auditor, churn in directors.

- All in all, it’s not an unusual story: sub-prime borrowers looking for funky and off-balance sheet financing which boosts free cash flow metrics, investors happy to pick up small amounts of income hoping that they won’t be hit on their large guarantee, financial innovation which seems mainly focused on avoiding regulation, and politicians willing to lend their name for a fee.

UK debt financings this week:

- Restaurant Group agreed terms for new loans with its banks (£120m) and a subordinated loan with an as-yet unnamed investor / lender for £380m – more details to follow.

- McColl’s added 1 year to its term loans agreed last year, pushing maturities to Feb-2024, as well as amending covenants and delaying amortisation.

- Blackstone’s Bourne Leisure borrowed the largest ever unitranche loan of £1.8bn, provided by Starwood, Blackstone and Apollo at L+550bp.

- Aggreko: TDR Capital and I Squared Capital’s £2.3bn buyout is being backed with £700m TL and £1bn of senior secured bridge loans.

- Diamond Transmission Partners raising a £1.1bn project financing for an electricity transmission link to the 1,218MW Hornsea 1 offshore wind farm in the UK.

- Western Power Distribution £350m credit facility.

- ICG Enterprise agreed a €200m RCF, replacing its existing €176m RCF.

Our services

Numis is an ambitious, dynamic and innovative investment bank, driven to excel across all aspects of its delivery.