-

BackWhat we doNumis is an ambitious, dynamic and innovative investment bank, driven to excel across all aspects of its delivery.Investment Banking

-

BackLatest newsRead the latest news about our business, our people and our work, find out about our next events and conferences.News

-

BackWho we areOur collaborative environment and distinctive way of excelling , is nothing without our great people.

-

BackOur board

Numis at a glance

Our Articles

28

Mar 2024

31

Jan 2024

Latest Transactions

London Stock Exchange Group PLC

£1.4bn

Co-global coordinator on the £1.4 billion sell-down of the London Stock Exchange Group PLC

March 2024

Custodian Property Income REIT

£237m

Sole financial adviser, sponsor and corporate broker

January 2024

Numis On Twitter

UK Hotel Market

Recovery prospects, the post-Covid market and the route back to peak revenue per available room (RevPAR).

If there’s one universal truth in hospitality it’s that certainty equals bookings.

As we emerge from the pandemic, and as governments allow progressive easing of restrictions, so the prospects for a recovery in hospitality rise.

The UK is recovering in phases. Consumers are already eating out more and having staycation weekends. Now, as the summer holidays play out they’ll spend more time in the stronger leisure markets, like Cornwall.

Later in 2021 we’re likely to see the corporate market come back, followed by long-haul.

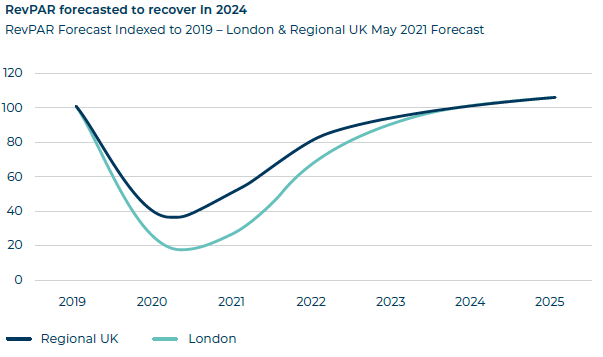

But it’s a long road. STR data indicate that UK RevPAR won’t return to 2019 levels until 2024.

UK hospitality is recovering – led by leisure demand

Four international markets are powering ahead: mainland China, Australia & Oceania, North America and the Middle East all have occupancy levels comfortably above 50%. Domestic travel is the backbone of all four.

Europe sits at the bottom of the pile with 29% occupancy and it also has the lowest RevPAR.

“What we can see from the UK perspective is quite positive. If we index occupancy on 2019, the US is back to 90% of where it was, China at 80% and the UK at 65% compared to the rest of Europe’s 50%.”

The UK starts to outpace the rest of Europe

Measured by the number of keys in the active pipeline, the UK remains Europe’s development hotspot with 150,000 rooms planned against second place Germany’s 100,000.

The lion’s share (42,000) are in London but the regions are well represented with Manchester developing 9,500 keys and 5,000 apiece planned in Liverpool, Edinburgh and Glasgow.

Premier Inn is likely to open 2,000-3,000 per annum, consistent with its longstanding 110,000 room target – a pre-Covid statement that remains a goal for Whitbread plc.

“We build our network strategy every few years, using multiple sources to obtain the most comprehensive view of market supply. Then we build a view of demand outlook across UK catchment levels, working with our property colleagues, and this is the model that leads us to the 110,000 number. In terms of where these rooms are, I’d expect a big contribution from secondary towns but overall it’s a patchwork quilt of opportunity.”

A two speed domestic recovery

Consumer

Overseas travel restrictions have created the perfect environment for domestic demand to thrive.

Many regions are performing well, with Cornwall, Devon, Dorset, Plymouth and Somerset all above 75% rolling seven day occupancy. The school holidays should provide more uplift.

But in gateway cities, the recovery is slower. Belfast and Cardiff, for example might be benefitting from weekend guests, but occupancy remains at just 60% and London lags badly at around 40%. This is something underpinned by history, which indicates smaller towns and suburbs usually return before bigger cities.

It’s also driven by consumers avoiding city hotels during the week. If domestic consumers do stay longer than a weekend, they’re more likely to do so in cities’ serviced apartments, where they can relax, cook and ultimately stay in as a family. Birmingham and Edinburgh have done particularly well here.

“Yet as the night-time economy reboots, you’ll see recovery in the bigger cities” adds Thomas Emanuel. And then after this, the international inbound market should return as restrictions loosen.

Corporate

We’ve seen some sectors, such as construction, travelling wholeheartedly.

But the broader, white collar market is yet to return. Businesses need to reboot their office space, bring in protocols, and welcome back their staff. It means a recovery creeping in over the summer before returning with more force from September

This is a segment in which Premier Inn, for example, continues to do well – thanks to its UK-wide network but also new partnerships with travel management companies, which provide a managed service to corporates that have complex travel requirements.

“The TMCs are very different to online travel agencies. There’s no cannibalisation and we get access to a corporate base we might otherwise be locked out of.”

Add all this together and you get steady recovery over the next two to three years with domestic consumer travel, followed by domestic businesses and rounded off by inbound international travellers.

All data is sourced from STR