-

BackWhat we doNumis is an ambitious, dynamic and innovative investment bank, driven to excel across all aspects of its delivery.Investment Banking

-

BackLatest newsRead the latest news about our business, our people and our work, find out about our next events and conferences.News

-

BackWho we areOur collaborative environment and distinctive way of excelling , is nothing without our great people.

-

BackOur board

Numis at a glance

Our Articles

28

Mar 2024

31

Jan 2024

Latest Transactions

London Stock Exchange Group PLC

£1.4bn

Co-global coordinator on the £1.4 billion sell-down of the London Stock Exchange Group PLC

March 2024

Custodian Property Income REIT

£237m

Sole financial adviser, sponsor and corporate broker

January 2024

Numis On Twitter

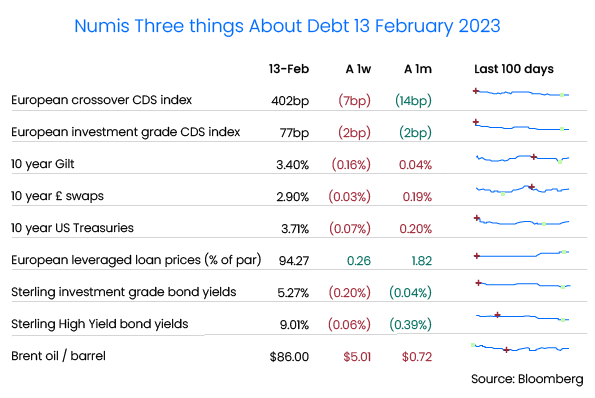

Debt advisory update

The end of January marked three years since Brexit finally happened, and it’s easy to agree with Lord David Frost that the ‘oven ready’ deal turned out to be an underdone turkey – though as its chef, he should know he could have changed the recipe.

30th January also marked the 90th anniversary of Hitler’s appointment as Chancellor of Germany and I recommend the series of podcasts by The Rest Is History on how quickly Hitler moved from being an also-ran to leading the largest party in 1932. In other democratic news, 31st January was also four years since Nadhim Zahawi’s problematic 2018 tax return was submitted.

Following our last article on Collateralised Fund Obligations, the FT then reported that US regulators are stamping down on this market, decreeing these bonds should normally be treated as equity; we welcome our readers from the FT and NAIC.

1. ESG wrinkles

In December, we closed a new £210m ESG-linked RCF for Tyman, after we advised on its $75m ESG-linked Private Placement bond earlier in the year, so it seems an appropriate time to reflect on where this sustainability linked loan (SLL) market is heading.

Simplifying massively, ESG has impacted the debt markets in three main ways:

- Some lenders are now curbing lending to oil and gas exploration (Danske and NatWest being the latest here, but there are many others).

- ‘Green’ bonds / loans, where there is a specific ‘use of proceeds’ e.g. a decarbonisation project

- ESG-linked debt, where the cost of debt goes down (or up) if ESG KPIs are (or aren’t) met. The amounts involved are not large – this study found that the average total change was up to around ±7.5bp for leveraged loans; it will be lower for investment grade loans, where credit margins are less than half of leveraged loans.

There are some bells and whistles on this; for example, any change in margin can instead be donated to charity, or the incremental cost could be implemented only at maturity – although this comes with its own problems: the optics of charities being seen to benefit from poor ESG performance are not great…

One key point is that, for lenders to count this as ‘ESG financing’, they need ongoing independent verification of whether the KPI has been achieved. We have seen some ESG advisers provide quotes of half or more of the potential interest saving, which does seem to raise the question of who is really benefiting here? I really do think there could quite easily be a different regime for listed (or regulated) companies vs private companies.

Margin changes bring other complications: under IFRS 9, a lender can book its loan asset at amortised cost only if its cash flows are solely payments of interest and principal. If its cash flows are driven by other factors (e.g. ESG achievements), then is there an embedded derivative in the loan? Should borrowers be doing the same?

The IFRS accounting body has suggested that ESG adjustments must be one of: (i) credit risk; (ii) profit margins; (iii) de minimis or non-genuine. The whole thing is a bit blunt, but worth a read…

Sometimes lenders can complain about the nominated charity: 9fin reported on a recent deal for Spanish theme park operator, PortAventura, which requested lenders make a 10bp donation to its in-house charity – this was ultimately dropped, partly because some lenders saw it a little like chugging.

We’ve also heard that the Loan Markets Association (LMA) will soon publish revised guidance on sustainability linked loans (SLL), including stricter ‘sleeping’ SLL provisions, where all the detail is punted to a future date, and advice to counter greenwashing.

This research found that ESG performance fell after ESG loan issuance, particularly where disclosure was poor, which is a little disappointing.

What next for ESG loans? Being a bit blue sky, perhaps good ESG performance could lead to improvements in the timing / quantum of final repayment? Would lenders consider slight relaxations in loan terms, such as greater acquisition flexibility or reduced information provision?

We did have one borrower suggest that its loan margin should be reduced if its bank’s own ESG performance was poor – if this had been in place in 2008-2020, some of our big banks could have ended up paying their borrowers.

2. Looooooong bonds

In January, European Energy issued another 1,000-year bond – we’ve talked about these ultra-long ‘hybrid bonds’ in the past (here) and it’s a bit of a cheat, since the bonds are designed to be refinanced in 4-5 years when the interest rate will reset to a punitive rate. (In passing, this year has seen a dissipation of investors’ worries about ‘extension risk’ for hybrid bonds, where they started to price these bonds to maturity instead of the earliest date of refinancing).

Setting aside perpetual bonds (of which Bloomberg tells me there are over 6,000 in issue), there are nine bonds currently outstanding that were issued prior to World War II, of which three were 100-year bonds issued by New Jersey’s utility in 1937 and five are from the Danish mortgage association Nykredit, with the oldest being issued in 1906, maturing in 2029.

But Bloomberg isn’t always right – the podcast A Long Time In Finance described a Dutch bond issued in 1648 and still paying a 2.5% coupon. This was issued by Hoogheemraadschap Lekdijk Bovendams (copy and paste there) to finance a new dam near the lower Rhine. 1,000 guilders of the bonds are held by Yale, which in 2015 sent its curator to Amsterdam to collect 15 years of interest, being €136.20 – full story here.

Apparently, even this is not the oldest bond, as this Hoogheemraadschap had first issued bonds in 1624, with the New York Stock Exchange currently holding a 1,200 guilder note. To put that in context, in 1624, the UK hadn’t yet had any kings called Charles and New Amsterdam (New York) was founded the following year.

It’s amazing that the Netherlands has had 400 years of sufficient stability for its legal and political systems to enable it to comply with the bond; in that time, France is on to its fifth Republic and Argentina had six military coups in the 1900s alone.

The other point is that inflation makes it much cheaper to do the hard work of ‘keeping your word’: today’s value of 1,000 guilders in 1648 is about $0.6m. But instead, 1,000 guilders is just $400, i.e. a 99.9% loss.

It’s also worth considering that, in Dutch and German, ‘Schuld’ means both ‘debt’ and ‘guilt’: debt is not a mere dry contractual relationship, it is laden with emotions and obligations that go beyond accounting. David Graeber is very good (if lengthy) on the link between debt and honour.

The other point is that inflation makes it much cheaper to do the hard work of ‘keeping your word’: today’s value of 1,000 guilders in 1648 is about $0.6m. But instead, 1,000 guilders is just $400, i.e. a 99.9% loss

3. A&E department

In a recent episode of the News Quiz, someone pointed out that really it should be ‘A or E’, or possibly ‘A and/or E’. But in this case it is definitely Amend and Extend: 2023 could be the year of the extension – not hair or houses, but the leveraged loan market, which mirrors what we saw in 2009-2012, when the first (?) leveraged finance bubble burst.

The basic idea is that some / all lenders agree to extend the loan maturity date in return for a change in economics – it’s mostly a loan thing; bonds typically use an exchange of new bonds for the old ones.

Some frills (there’s a bit of game theory going on):

- Forward starting loans: if only some lenders want to extend, then there is a new (higher priced) loan for just these lenders, starting at the current maturity date and ending a couple of years later. Non-extending lenders are run right to the end of the cheaper loan, rather than being refinanced early.

- Exit consents and covenant stripping: this works when the majority of lenders are happy to extend: a nanosecond before the consenting lenders are refinanced into a new tranche, they consent to remove rights for those lenders left behind. Thanks to a legal case called Assénagon, this is more difficult in the UK than elsewhere, but still possible.

- There is also“creditor on creditor” violence, where some lenders will extend / lend more if they can screw other lenders by better terms, or more equity upside.

There have been several big ‘vanilla’ A&E deals this year, with the biggest so far being a €8bn-eq deal for Altice France (SFR) that pushed out 75% of its 2025 and 2026 maturities to August 2028. Despite not being ‘new money’, these can give interesting insights to the market:

- Pricing movements: margins moved from 275-300bp up to 550bp and a 2pt discount to par (98 OID).

- Existing lenders are happy to extend at only a modest discount to par (maybe 3pts vs the 7pts that a new deal would have needed). Some of this is because the ‘Amend & Extend’ means some existing CLO lenders can retain these loans rather than having to return any repayment proceeds to their own investors.

- Strong demand from new investors: Altice raised €150m of new money.

- Tighter documentation terms: closing ‘trapdoors’ that enabled sponsors to steal collateral and reducing debt incurrence.

INEOS has also been in all financing markets: it’s raised €3.5bn for its new plant in Antwerp (of which €1.2bn is coming from UK, French and Spanish export credit agencies) – fair play, Jason. INEOS has also raised €2.6bn in loan and bond markets, of which €2.1bn refinanced existing 2024 debt and the rest can contribute to Jim’s fund to buy Manchester United.

4. Bonus feature: Are private credit funds diversified enough?

This may be niche, but caught my eye: diversification is known as the only ‘free lunch’ in finance: if assets are not perfectly correlated, then a small amount of diversification will increase returns without increasing risk.

For equities, the standard thinking is that about 30 stocks are enough for a portfolio to be sufficiently diversified, where the big winners offset the big losers.

For a credit investor, there are still zeroes, but there are no ‘big winners’: the best a lender can get is interest and par repaid – lenders’ returns are more ‘skewed’ than equity returns.

Private equity averages about 15-23 investments per fund and private credit funds are even less diversified: a study by Arena found that the average fund had just five investments. This may even overstate diversification if managers specialise in just a few industries. Perhaps the transaction and surveillance costs of putting in place a truly diversified fund are just too great.

One study suggests that optimal diversification for a portfolio of ‘skewed’ investments like credit could well be close to 100 investments. As Arena put it, “This free lunch often proves too costly to eat”. The implication is that many funds will be hit sideways by one big loss – would love to hear from any private lenders out there.

Recent UK debt deals

Loans

- Virgin Media O2 wrapped its £3.25bn loan financing to expand the cable network to new homes. This was underwritten by Barclays last summer, so they must be relieved to see it off their books.

- Heathrow refinanced its £1.15bn revolver into a new 4+1+1 deal, with 21 banks. Four banks dropped out and two joined.

- Fintel refinanced its £80m four-year revolver, with Santander joining NatWest and Virgin Money (rarely seen in UK corporate loans).

- Gentoo (housing association) obtained an A-rating from Fitch and agreed £460m of loans and a 40-year private placement.

- Astra Zeneca added a further $2bn of bank facilities, on top of its previous $4.9bn of relationship RCFs.

- Endava (software and services) closed a £350m RCF with HSBC, DNB, NatWest, BBVA, KeyBank and Fifth Third. Silicon Valley Bank appears to have exited.

Leveraged finance

- Rubix extended €1.19bn of term loans.

- INEOS extended €2.1bn of debt, raised €0.5bn more and raised a further €3.5bn project financing for its new plant, with plenty of export credit backing.

- Safetykleen refinanced €490m of EUR term loans and pre-placed €120m-eq term loans. GBP was about 75bp more on margin, but same OID.

- Tikehau is providing £95m term loan and £20m capex line for Sun Capital’s buyout of K3, along with £30m super senior loans from PNC.

- Agrekko is adding €410m-eq to its debt, pricing TBA.

Investment grade bonds

- Vodafone and BP both accessed the USD markets, with BP raising $2.25bn at 4.8% and Vodafone raising $1.2bn at about 5.7%.

- BT raised £350m of 18-year sterling bonds at 5.75% (G+200bp), which is about 0.25% higher than secondary levels. This is on top of €800m of EUR at 3.75% (swaps+93bp).

- Northumbrian Water raised £350m of eight-year bonds at 4.5% (G+145bp) – this compares to 6.375% for the bonds it raised in November.

- The AA completed the liability management exercise it started last summer, issuing £400m of five-year bonds (BBB just) at 8.45%, which is about 50bp wide of secondaries. This has tightened significantly since, with its credit spread now 454bp, about 80bp lower than issue.

Disclaimer

This briefing has been prepared using publicly available information and should not be relied upon for any investment decision. Numis does not make any representation or warranty, either express or implied, as to the accuracy, completeness or reliability of the information contained in this briefing. Numis, its affiliates, directors, employees and/or agents expressly disclaim any and all liability relating to or resulting from the use of all or any part of this briefing or any of the information contained herein. This briefing does not purport to be all-inclusive or to contain all of the information that recipients may require. The information contained herein is subject to change and Numis accepts no responsibility for updating it.

Our services

Numis is an ambitious, dynamic and innovative investment bank, driven to excel across all aspects of its delivery.