-

BackWhat we doNumis is an ambitious, dynamic and innovative investment bank, driven to excel across all aspects of its delivery.Investment Banking

-

BackLatest newsRead the latest news about our business, our people and our work, find out about our next events and conferences.News

-

BackWho we areOur collaborative environment and distinctive way of excelling , is nothing without our great people.

-

BackOur board

Numis at a glance

Our Articles

28

Mar 2024

31

Jan 2024

Latest Transactions

London Stock Exchange Group PLC

£1.4bn

Co-global coordinator on the £1.4 billion sell-down of the London Stock Exchange Group PLC

March 2024

Custodian Property Income REIT

£237m

Sole financial adviser, sponsor and corporate broker

January 2024

Numis On Twitter

Debt Advisory Update

This month has seen the 25-year anniversary of the ‘independence’ of the Bank of England, just days after the historic election that brought Tony Blair to power. Gordon Brown’s prolix letter setting out the framework which is long on price stability and short on quantitative easing. In other news this week, the Governor of the Bank of England warned of “apocalyptic” food price rises and inflation over 10%, which is still better than the 15% inflation at the Queen’s Silver Jubilee in 1977.

TL / DR: Deleveraged Markets; Default ≠ Default; Dynastic Debt

1. Deleveraged markets

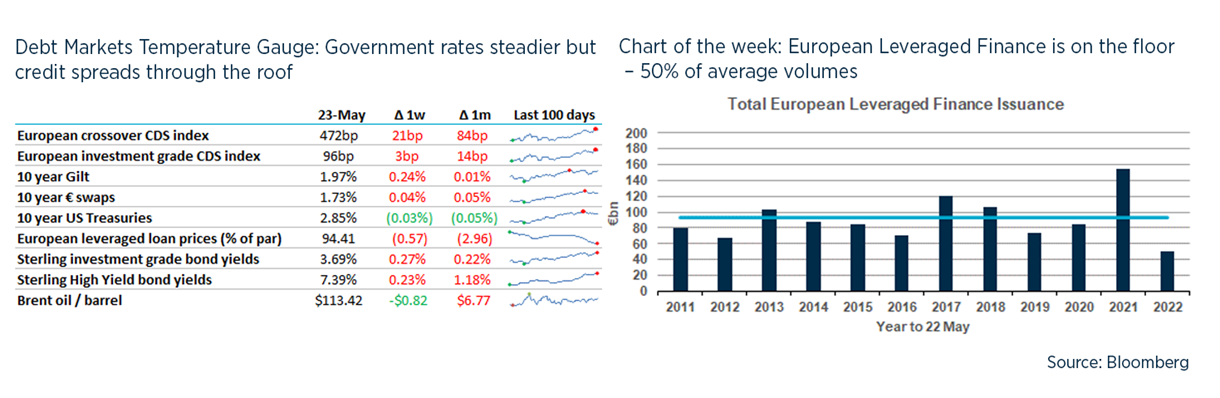

- For many years now, the main two themes of global credit markets have been (1) impossibly low government rates and (2) vibrant leveraged finance markets, being one of the few places where investors can find some yield.

- It should come as no surprise then that when (1) reverses, (2) also falls away. For much of 2022, European high yield markets have been even quieter than Manchester United fans, with only three issues in the past 3 months (and two of these are bid below the initial price).

- Like Wile E Coyote hovering above the precipice, the leveraged loans market was the last holdout: these are floating rate and so investors can benefit from rising rates. But only until investors get concerned that higher rates will crash the economy and impair credit, and so last week this market rolled over too, with a € / $ cross-border loan deal for Optigroup being pulled after launch.

- As the chart above shows, European leveraged finance is running almost 70% below 2021 volumes and 50% below the average of the last 10 years.

- This is bad news for banks still holding stuck bridging loans for deals announced in 2021 e.g. £1.7bn of debt underwritten for 888’s acquisition of William Hill’s international business not to mention the remaining £2.7bn of Morrison’s acquisition debt.

- Banks are now unwilling to underwrite new deals for wider syndication, or if they are willing to propose terms then can include so much price flex as to be too expensive.

- Instead, the very last leveraged investors standing are the debt funds which, like the private equity funds, have committed undrawn dry powder that will earn them more fees if it is deployed – and investors cannot ask for it back or easily refuse a capital call.

- These debt funds are feasting, taking alternate bites from banks’ hung bridge books (like Morrison’s secured high yield bond), new deals – sometimes in a club (like 5 funds providing £240m to Apax to buy Alcumus or TA refinancing The Access Group) or just buying beaten-up secondary deals from loan funds that have been facing redemptions.

- With the debt funds being the only game in town, many bigger deals will be clubbed between several funds. It’s not easy to put together a club for an acquisition, and balance sheet banks will be faced with a decision of whether to become a non-independent debt adviser to arrange these deals or even to underwrite to a new ‘market’ for distribution, like Barclays is rumoured to be considering for TDR / Issa’s bid for Boots.

- But the problem here is that private credit is supposed to be bespoke and one of the main credit protections is that the fund is the only lender and controls the position. If neither of these is true then are private credit LPs really getting what they are paying for?

- Perhaps GPs might propose that the option value of liquidity is illusionary and instead investors are better served by committing to maintain investments even when markets are bad, a bit like consistently dollar-cost-averaging. With locked-up capital, it’s impossible to pull your funds out when markets collapse.

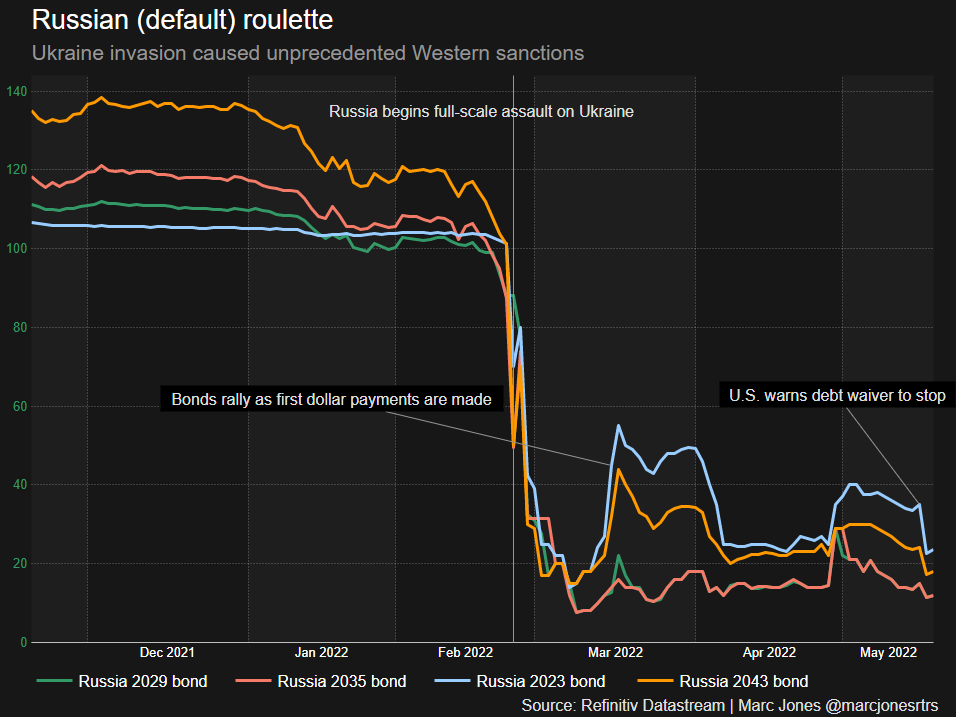

2. When is a default not a default?

- When I was a lending banker, I would occasionally hear clients explain that the only reason they remained in default is because the banks wouldn’t waive the necessary covenants.

- Banks have an ambiguous relationship with financial covenants: there is a school of thought that covenants provide false hope to lenders and that actually value is better maximised if lenders forego the ability to meddle in management that financial covenants can enable – I suspect we will find out over the next year.

- Borrowers are often best served by maintaining that there has not yet been a default for as long as credibly possible. A group of lenders can unilaterally determine that there has been a default even if borrowers deny it but this typically requires at least 25% of lenders to instruct the agent to declare a default. So in the first instance, the lenders will often look to the borrowers to come clean.

- So the question of “Is Russia in default of its bonds?” turns out to be “depends who you ask”.

- The ratings agencies: “of course”, and they have since withdrawn ratings.

- The market: “we’re marking the bonds at 20c/$ so practically yes”.

- ISDA’s Determinations Committee (which decides if the CDS is triggered): “nearly, but not yet”.

- Russia: “Nyet”, because they keep sending money over to the banks responsible for clearing the coupon payments. When the initial payments were blocked, Russia first offered to pay in Rubles then used US$ outside the US’s sanctions. The next test will be after in June, when the US government ends its licence for bondholders to receive funds from Russia on 25 May.

- The German real estate company Adler shows how long an issuer can refusing to admit a default. Some background first: Adler is in dispute with several short sellers, especially Viceroy Research led by ex-social worker Fraser Perring, who was previously one of the first to identify problems at Wirecard and Steinhoff. In response to Viceroy’s reports, Adler commissioned a segregated team at its auditors KPMG to investigate the allegations. KPMG published its inconclusive report in April (FT article here).

- Adler’s bonds contain an obligation to deliver “within 120 days after the end of each of the Issuer’s fiscal year, audited consolidated financial statements”. So at 30 April, investors eagerly awaited the accounts and KPMG’s audit opinion. Instead, they learnt that KPMG had issued a “disclaimer of opinion” – Adler maintains this means it has published “audited accounts” whereas others point to the International Standard on Auditing which suggests a disclaimer is an alternative to resigning as auditor.

- This one might run & run – but not with KPMG which Adler sacked last week, only an hour after it told investors it wanted to keep KPMG as its auditor. Must have been a busy 60 minutes

- Adler no longer has just friendly banks as creditors and the latest Bloomberg headline is “Hedge Fund Groups Pick Lawyers to Strategize on Adler’s Debt” which I suspect means they are not taking Adler’s word on this.

{kind=link}

3. Dynastic Debt

- While checking out something for a client recently, I came across what I thought at first was a typo: in 2021, the Danish utility Ørsted issued a Sterling bond at 2.5% which matures in February 3021. Yes, 1,000 years after being issued. Ørsted has form here – this is a slightly longer maturity than its 3013, 3017 and 3019 bonds. I assume they have staggered the dates to avoid those troublesome maturity clusters.

- I tried to find out what might happen in 3021. I could be 1,045 years old. A US president could be taking office after the election in the previous November. £1 at 3% p.a. compounded would be £6.6n. Easter will be late, on 22nd April.

- More importantly, on 18th February 3021, if not already repaid by then, Deutsche Trustees will start the wheels turning on sending £425m to various investors (or whatever Star Wars currencies are in use by then – just now, it seems very unlikely that the UK will survive that long). I’m hoping Linklaters has lined up Mr Slant or the Grail Knight to monitor the process.

- Of course, the bond is structured this way to be something other than perpetual (in which case it would be equity and so not tax deductible) and ordinary debt (in which case the ratings agencies would not treat it as 50% equity). Like most corporate hybrids, it has features that will incentivise but not compel the issuer to refinance after 10 years, after which the deferrable coupon will be reset to a slightly higher rate. But theoretically, the bond could be outstanding for the rest of recorded time.

- Of course, this is a Green bond, since Ørsted needed to do its bit to ensure the world will survive long enough for them to get repaid.

- Hybrid bonds are usually the preserve of large utility and natural resource groups, although National Express was a notable mid-cap issuer in 2020, with a perpetual £500m note to preserve its investment grade rating.

- Most issuers opt for maturities of 50-100 years, which is deemed sufficiently far away for “I’ll Be Gone, You’ll Be Gone” to apply – effectively perpetual but legally finite. But for tax reasons, Danish issuers have taken this to the extreme. I’m not clear why 1,000 years is viewed as better than say 500 years but 2,000 years would be right out.

- Interestingly, given current yields in the market, there is currently no incentive for Ørsted to refinance this bond in 2031 as it will be cheaper to pay the slightly higher reset rate. We will find out in 9 years time – I know how to finish on a cliff-hanger…

Recent UK Financings

Loans

- Gateley agreed a £30m 3-year RCF with Lloyds and HSBC at SONIA +195bp, up from £8m.

- Clinigen dropped its sterling tranche of its leverage loan and replaced it with EUR.

- Barclays arranged a novel ABL loan for Aurelius’s acquisition of Lloyds Pharmacies – structured of the government receivables due to the chemists, the banks rolled over a previous arrangement (Barclays, ABN, BNP, HSBC, NatWest, Secure Trust Bank).

- Redcentric signed a £80m RCF at SONIA +175bp with an upfront fee of 0.75%, with NatWest, Barclays, Bank of Ireland and Silicon Valley Bank.

- Boohoo signed a £325m 3-year RCF.

- InterContinental Hotels Group signed a $1.35bn 5-year RCF.

- Apax Global Alpha increased its evergreen RCF to €250m with Credit Suisse making a rare appearance in this section.

- EuroCell refinanced its £75m sustainability linked RCF to 2026.

- 6 out of Britvic’s 7 banks extended its RCF by +1 year.

- Peabody agreed a £75m 5-year RCF.

- British Land added £100m 5-year bilateral to its £450m 8-bank RCF.

- Future plc increased its loans again by £100m, now to £620m and extended to 2025.

- Brookfield has lined up £1.2bn to back its acquisition of HomeServe, provided by Bank of America, Deutsche Bank, MUFG and Royal Bank of Canada. This will probably be taken out in the investment grade or infrastructure loan market.

- Next 15 increased its loans to £!50m for the agreed acquisition of M&C Saatchi, with HSBC stepping up.

- Judges Scientific has agreed £80m of 4-year loans for its acquisition of Geotek, from Lloyds, Santander and Bank of Ireland.

Bonds

- Miller Homes priced the first high yield bond since January: 7% 7-year priced at a discount to yield 8.25% - now trading to yield 8.9%. This was alongside a EUR 6-year floater to appeal to loan investors, at E+525bp again priced at a discount of 97. The banks had been sitting on this commitment since December …

- Carnival went back to the future and priced a $1bn 8-year high yield bond at 10.5%, pricing which was last seen in the aftermath of the crisis in 2020.

- Housing Association Jigsaw priced £250m of 30-year sustainability bonds at G+157bp

- Jersey priced £500m of 30-year bonds at G+100bp (so it turns out Jersey is safer than houses).

Our services

Numis is an ambitious, dynamic and innovative investment bank, driven to excel across all aspects of its delivery.