-

BackWhat we doNumis is an ambitious, dynamic and innovative investment bank, driven to excel across all aspects of its delivery.Investment Banking

-

BackLatest newsRead the latest news about our business, our people and our work, find out about our next events and conferences.News

-

BackWho we areOur collaborative environment and distinctive way of excelling , is nothing without our great people.

-

BackOur board

Numis at a glance

Our Articles

28

Mar 2024

31

Jan 2024

Latest Transactions

London Stock Exchange Group PLC

£1.4bn

Co-global coordinator on the £1.4 billion sell-down of the London Stock Exchange Group PLC

March 2024

Custodian Property Income REIT

£237m

Sole financial adviser, sponsor and corporate broker

January 2024

Numis On Twitter

Debt Advisory Update

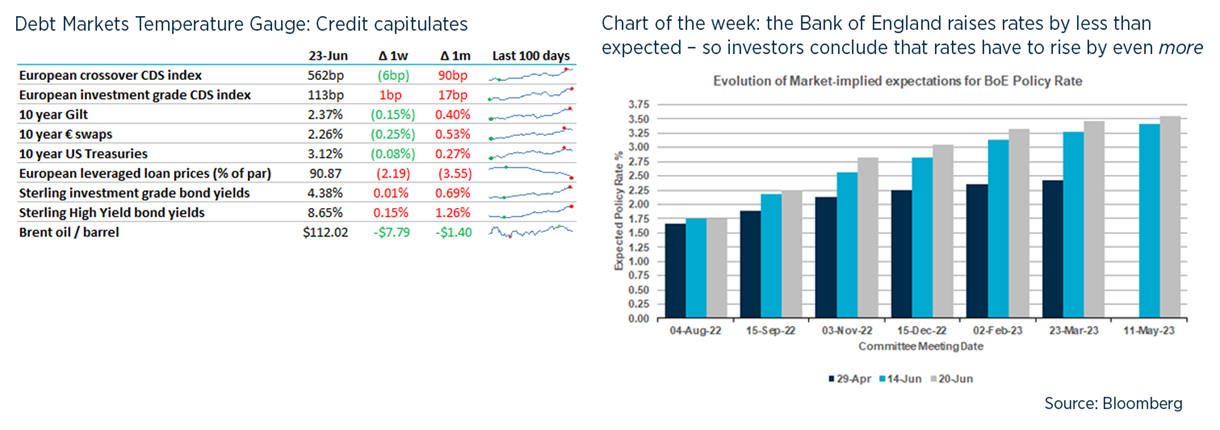

Since we last wrote, the world has realised that inflation really is ‘a thing’. Currently UK CPI has reached 8.6% but for like-for-like comparison, RPI is now already 11.1%% (while RPI is bad statistics, pension funds are current suing the Govt to reinstate this for index-linked bonds).

So last week, we saw the Fed raise by 75bp, leaving the Red Funds Rate at 1.75%, well below its level throughout the 1990s. While the BoE was expected to raise rates by at least 50bp, instead they opted for 25bp, deciding that base rates of 1.25% is enough to quell inflation; for reference, this means that UK real rates are now -ve 7.25%. It’s good to see the Bank of England having its independence tested but, like my waiting for my children’s end of year exam results, I’m worried about the outcome.

TL / DR: Leveraged finance reborn; Liquidity as an option; Russia defaults, again

1. Syndicated Leveraged Credit – The King is Dead, Long Live The King!

- We have discussed with clients and colleagues alike where the credit markets are right now: in short, a typical UK investment grade bond issuer like Rentokil (BBB) is paying >5% to issue 10-year sterling bonds while any high yield issuer would have to be considering much closer to 10%.

- In the meantime, we may have seen a revolution in leveraged finance markets. For many years, any deal between say £50m and £250m has been best executed through a private debt fund. Often, this size would be possible with a single lender, docs are bespoked (particularly covenant definitions) and if there was a maintenance covenant then it was loose with plenty of headroom.

- Deals bigger than this often went to the leveraged loan and high yield markets.

- What’s changed? Leveraged finance markets in Europe are if not dead then comatose, particularly sterling. New issuance volumes in European leveraged finance (HY + loans) are down by 65% year on year. There have been a handful of deals (eg Manuchar) in recent weeks which have priced €350m at a 86c / € to yield >11% - and this is apparently after a debt fund took €75m before launch.

- 888 is in the market now with £1.4bn of EUR high yield bonds and USD / GBP loans to fund is acquisition of William Hill’s international business. This was underwritten by JPM and others back in September so it may well entail a large loss for the banks – let’s see where it prices.

- Given this, even deals above £100-500m are now being done by debt funds. The poster child (and kudos to TA Associates) is the £3.5bn club of >15 direct lenders for The Access Group.

- This could be good news! Instead of paying investment banks to provide bridge facilities / underwrite leveraged loans and high yield bonds, borrowers (or their advisers) can instead put together a club of happy lenders from day 1.

- But I think there are a few wrinkles.

- Is it really feasible to put together a club of supposedly bespoke lenders for a time-pressured P2P? In particular, this could cause problems for a UK deal subject to the Rule Of Six.

- Time and complication: The Access Group deal was ‘announced’ on 12 April aiming at closing by 30 April, which is 5 weeks earlier than the announcement date of 8 June. In mitigation, there was a lot going on, between terrible markets and a complicated piece of M&A / corporate finance. There have been other private deals funded by debt funds such as Envirotainer and CordenPharma.

- Is this really what direct fund investors are paying their fees for? They were promised differentiated, bespoke, senior-secured credit exposures paying >7% where their managers would be in full control. Instead, they are participants in a club loan deal paying S+525bp.

- The logical next step is for the investment banks to underwrite debt with the intended primary syndication being to debt funds. This is a continuation of the ‘accidental’ distribution of stuck positions to funds e.g. Morrisons. The first deal in Europe to be done this way was announced this week: Norgine, where Goldman Sachs is leading Jefferies and KKR in underwriting €650m of debt to be marketed to “20-30 debt funds this week and next”.

- While I applaud their innovation, I can’t see this being practical for a more normal deal flow of 10-20 new leveraged deals per month. Or at least, the debt funds are going to have to step up their resourcing, or rely more on public credit ratings – which is inconsistent with their sales pitch to LPs.

- This will also significantly reduce public disclosure for leveraged deals. In terms of ranking of transparency, if High Yield bonds are as clear as vodka and leveraged loans are a glass of rose, then private loans are a pint of stout in a ceramic tankard.

2. Pricing the liquidity premium

- This piece by Cliff Asness got me thinking about the liquidity premium – the old-fashioned idea that investors should get a higher yield for illiquid assets like private equity to compensate them for the inability to realise their investment in short order. A counter-argument for this is that investors are better off investing in illiquid assets because they are unable to make the classic mistake of selling out after prices have fallen: they are forced to remain invested, as explained on page 3 here.

- Maybe we should think about liquidity as a call option to freely swap your assets for cash. The ‘underlying’ in this case is the requirement for or ability to use that cash. Googling suggests this may not an entirely original idea!

- What does financial theory say are the key drivers of option value and how have these changed in the past six months?

- Value of the underlying: seems pretty clear to me that the world is a much more difficult place than it was in December and that this has increased the utility of having a cash buffer for emergencies e.g. Ukraine, volatile equity markets gyrations, political instability, supply side shocks. Put another way, having cash better equips you to deal with tricky situations or take advantage of opportunities.

- Volatility of the underlying: again, not only is the world a more difficult place but I think the volatility of changes in outlook has also increased. The Economist thinks that 2019 Q4 was more uncertain than Q1 this year but I’m not sure I agree.

- Interest rates: classically, higher rates increase the value of a call option, because you get the upside from price increases without laying out cash for the full amount of the notional. Interest rates are also the price / value of cash: when rates are zero and credit is easy, it doesn’t matter if you can’t realise your illiquid asset as you can always borrow to get cash. When rates are high, cash is king.

- Time to expiry: Not sure about this one to be honest; suggestions welcome.

- Looking at it this way suggests that the liquidity premium could well have been close to zero in recent years but now the illiquidity premium should be much higher.

- If this is right then private / illiquid assets should be marked down by more than listed assets, not less.

3. Is Russia in default? (ctd)

- This may well be a running topic, like Citi’s Revlon mistake.

- Incidentally, Citi’s embarrassment was in the FT again this week as Revlon filed for bankruptcy, forcing the issue of whether Revlon actually owes anyone the $500m that Citi mistakenly paid to its lenders. Citi certainly believes that it would be able to get this back from Revlon but it’s not proven yet.

- Credit Default Swaps pay out upon if the reference entity “defaults” on its bonds, and default is determined by the CDS Determinations Committee of ISDA (International Swaps and Derivatives Association). This is made up of 14 investment banks and large investors. Usually decisions are unanimous as it’s clear whether there has been a default. In this situation, although the committee found there had been a default, Citi disagreed and Cyrus Capital didn’t vote at all. As Citi is the agent on the bonds, perhaps it has had more conversations with Russia about how to pay the coupon without triggering sanctions.

- As a recap: Russia failed to repay its $2bn bonds due in April but somehow managed to get USD to Citi in May before the end of a 30-day grace period. So, no default there.

- However, some bright spark noticed that Russia should also have paid interest on the overdue amounts and that the grace period for paying this expired on 19 May. So there was a failure to pay and therefore Russia is in default under its bonds. The full reasoning is here.

- Pride goes before a fall: some have speculated that Russia didn’t pay the default interest because it didn’t want to acknowledge it had defaulted. But now it really has defaulted precisely because of not wanting to acknowledge its default.

- Normally, there would be an auction to work out how much CDS holders will receive but this is a weird situation as (a) sanctions have been toughened up, so that it is now illegal for US investors to even trade Russian debt (b) these particular bondholders didn’t really lose a cent. The auction has been deferred while everyone puts on a cold towel and tries to work out what to do.

- With Russian bonds trading at 35c / $, some investors will be keen to maximise payouts. Pimco has already lost $400m on its CDS and could lose much more. Watch this space.

Recent UK deals

Loans

- Moonpig added £60m to its RCF to fund its acquisition of Buyagift.

- Next 15 added £80m to its debt to part-fund its potential acquisition of M&C Saatchi, provided by HSBC and Bank of Ireland at SONIA + 235bp.

- Inspired Education added €250m incremental leveraged loans at E+450bp and an OID of 97.

- Manchester Airport refinanced its £590m RCF and securitisation liquidity lines with NatWest, BNPP, Barclays, CIBC, NAB, SMBC and Handelsbanken.

- Fullers refinanced £220m term loan and RCF at SONIA +285bp out to 4 years.

- CityFibre has agreed £3.9bn of loans to fund its rollout through a deal underwritten by NatWest, SocGen, Credit Agricole, BBVA, Intesa Sanpaolo, ING and SEB, with ABN, Lloyds and M&G joining.

- Aquila increased its RCF from €40m to €100m to fund acquisitions.

- GSK’s Haleon Consumer Health business agreed £3.6bn of loans from a large syndicate.

- DiscoverIE increased its revolved from £180m to £240m and extended it to 2025.

- Whitbread renewed its £775m RCF (down from £850m previously) out for 5 years. Santander, Barclays, NatWest and Bank of China are some of 7 banks providing this.

- Halma refinanced its £550m RCF and extended it to 2027.

- Capital & Counties agreed a £576m loan to backstop change of control provisions in its bonds following its merger with Shaftesbury. Barclays, BNPP and HSBC are providing this, for up to 3 years at SONIA + 150bp.

- Homeserve’s acquisition by Brookfield is backed by a £1.2bn bridge facility from Bank of America, Deutsche Bank, MUFG and RBC. This will be refinanced shortly after the takeover.

- Ocado announced a new £300m RCF alongside its £575m equity placing.

Private Placements

- Segro announced €225m of 10- and 20-year private placements in EUR at a yield / spread of 3.87% / 133bp for the 10-year and 4.14% / 170bp for the 20-year.

- Halma also agreed a £330m private placement in USD, GBP, EUR and CHF with a 7-year average life.

- Custodian REIT announced a 10-year £25m private placement with Aviva at 4.10%.

Bonds

- The arrangers of CD&R’s Morrison’s debt sold the EUR High Yield to Pimco at a significant discount and are looking to syndicate more of the hung bridge debt to Asian banks.

- Rentokil priced $2bn eq of EUR and GBP bonds are average coupon of 4.4%, about 6x what would have been expected when its acquisition of Terminix was announced.

Disclaimer

This briefing has been prepared using publicly available information and should not be relied upon for any investment decision. Numis does not make any representation or warranty, either express or implied, as to the accuracy, completeness or reliability of the information contained in this briefing. Numis, its affiliates, directors, employees and/or agents expressly disclaim any and all liability relating to or resulting from the use of all or any part of this briefing or any of the information contained herein. This briefing does not purport to be all-inclusive or to contain all of the information that recipients may require. The information contained herein is subject to change and Numis accepts no responsibility for updating it.

Our services

Numis is an ambitious, dynamic and innovative investment bank, driven to excel across all aspects of its delivery.