-

BackWhat we doNumis is an ambitious, dynamic and innovative investment bank, driven to excel across all aspects of its delivery.Investment Banking

-

BackLatest newsRead the latest news about our business, our people and our work, find out about our next events and conferences.News

-

BackWho we areOur collaborative environment and distinctive way of excelling , is nothing without our great people.

-

BackOur board

Numis at a glance

Our Articles

28

Mar 2024

31

Jan 2024

Latest Transactions

London Stock Exchange Group PLC

£1.4bn

Co-global coordinator on the £1.4 billion sell-down of the London Stock Exchange Group PLC

March 2024

Custodian Property Income REIT

£237m

Sole financial adviser, sponsor and corporate broker

January 2024

Numis On Twitter

Debt Advisory Update

What a summer of live action! Hot on the heels of England’s amazing cricket revival (in the Test form at least), we’ve had Wimbledon, sparkling rugby internationals, Women’s Euros and now the Tories have decided to play It’s a Knockout for the next couple of months.

Keep safe in the heat – I’m expecting a pretty full house in our air-conditioned office tomorrow.

TL / DR: A bridge to somewhere; Banks taking a bath on credit underwrites; In God we trust

1. A bridge too far

- There have been a couple of bridge loans recently that highlight the different form of bridges – and what exactly a “bridge loan” is altogether.

- Usually a bridge loan is a short-term arrangement to facilitate moving from one situation to another. And like a stepping stone, you wouldn’t want to pause there for too long.

- Rentokil’s financing for the acquisition of Terminix announced in Dec-21 was a typical example of an “investment grade bridge”: a $2.7bn bridge loan that was subsequently refinanced into a $700m 3-year term loan and a $2bn 1-year bridge to bond issuance (probably with Rentokil having the ability to extend by 6 months).

- But the key here is that the bridge is just a short-dated loan: the lender has no direct risk on what follows – so when Rentokil went to market in June to refinance the loan with $2bn of bonds, the fact that it was much more expensive to issue was Rentokil’s problem, not Barclays’.

- Barclays would care if Rentokil was unable to issue or unwilling to take the market price, but the bridge is short-dated and contains economic incentives to refinance early, such as escalating pricing or fees after 6 or 12 months. Very rarely in investment grade, a bank will insist on a “go to market” clause which forces the borrower to issue if possible – this is much more common in leveraged loans.

- Investment grade markets are much more reliably open than leveraged markets, and pricing tends not to move so much. So the borrower and lender are pretty comfortable that it will be taken out asap. And Rentokil did this: only 4 months after signing the bridge, it was in the market – despite having to pay much higher than envisaged at the time when it announced the deal (maybe $75m p.a. more in interest).

- Bridges start cheap and then get very expensive: bankers always say “we’re in the moving business, not the storage business”. They’re happy to provide a short-term bridge to win the capital markets business.

- The other sort of bridge is what 888 had for its acquisition of William Hill’s non-US business: a short-term loan that the banks aim to refinance into institutional loans or bonds. However, if the banks can’t do this then the bridge flips automatically into extended loans or exchange bonds which the banks have to hold – or then sell at a loss. There’s a good summary here.

- So long as 888 complied with its obligations to help the banks sell the loans, it faced no market risk – the banks had guaranteed the maximum rate on the loans / bonds and if that wasn’t enough for investors then the banks had to discount the debt even more until the yields were attractive enough.

- There are other bridges such as a bridge to a disposal like Issa / TDR used for Asda, or a bridge to target cash, like we used in LTG’s acquisition of GP Strategies last year. Or even equity bridges, which no-one likes much.

- Or there’s this very weird deal: in February, Morgan Stanley provided a $2.7bn “backstop” for Royal Caribbean: MS has agreed to refinance, repurchase or repay bunch of RC’s debt falling due in 2023 and RC has the right to sell up to $3.15bn of 5-year unsecured notes to MS in Q2 next year. This has enabled RC to state it no liquidity risks. What’s weird is that there appears to be no cap on the cost of the debt for RC, which makes it less than perfect for Royal Caribbean. It wouldn’t surprise me if MS has bought CDS on Royal Caribbean to hedge its market risk somehow.

- Takeaway: if you’re going to use a bridge, make sure you know where it leads.

2. Taking a bath

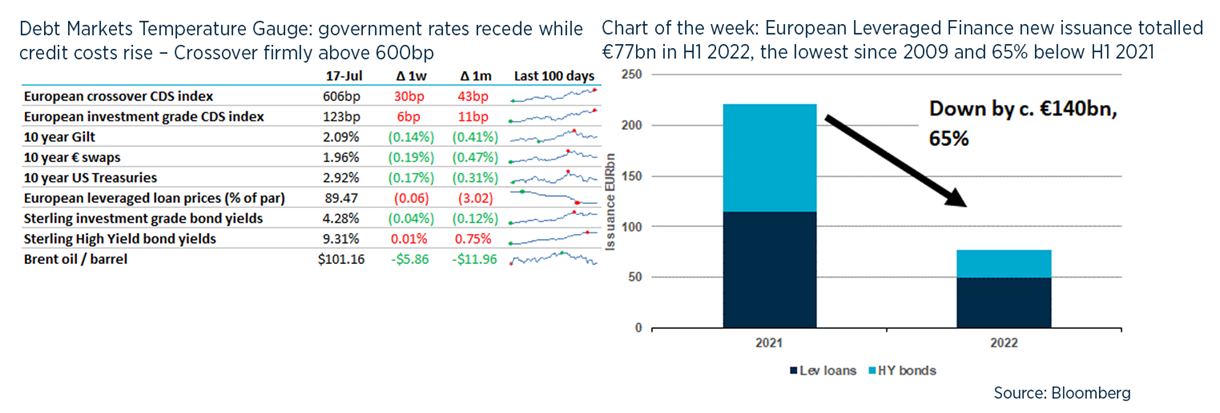

- We talked last time about how the closure of the leveraged finance markets has provided an opportunity for the debt funds to step up – and for the bolder investment banks to underwrite with the intention to distribute to these funds.

- As shown in the Chart of the Week, European leveraged finance new issuance volumes are €140bn lower than H1 2021 – this is leading to extreme congestion in debt funds, as the “only game in town”. And we’re now seeing debt funds respond to this by slowly increasing pricing (maybe +100bp since earlier this year), demanding more robust covenants and being increasingly selective.

- The past few weeks have shown the extent of the losses for the underwriting banks are taking on hung deals (assuming fees of 2.5% in each case).

- 888: JP Morgan and Morgan Stanley led a group of 4 banks providing c.$2bn in Sep-21 of which c. $1.2bn was sold down at 85% of par, indicating a loss of c. $150m. The banks also retain c. $750m of debt which they are probably not marking-to-market, thus avoiding another $94m of losses.

- Credit Suisse sole underwrote €350m of debt for Manuchar which it sold at 86 – implied a loss of €40m.

- Citrix has $15bn of debt to distribute, with caps priced in January. If this were sold at 10pt loss then this could generate cash losses to banks of $1-1.5bn.

- Morrisons – it’s not been easy keeping track of the losses incurred by the underwriting banks as they’ve dribbled the deal out since January. Bloomberg estimates £125m of losses, with £2.2bn of debt left to be distributed (implying a further £200m+ of losses).

- JP Morgan’s Q2 results included a charge of $257m for markdowns to its bridge book.

- And finally of course, there $13bn of debt for Musk’s on/off acquisition of Twitter, where losses could exceed $100m.

- As 888 made clear this week, in the leveraged finance market, the losses fall onto the underwriting banks that had guaranteed the availability and maximum cost of funding, and not on the borrower. But it still matters for borrowers.

- A bank that has taken a huge cash loss on an underwriting may not be a reliable partner in the future. While some banks may dispute this (“we always stand by our clients” etc), it’s easier to see if it’s turned around the other way: banks that have made £100m+ in fees are going to regard their borrower as a more valued client. At the very least, the banks are likely to regard the borrower as morally obligated to provide more future business to make up the loss.

- Banks with huge hung commitments are going to be unwilling to put on new risk. We saw this with the aborted bid for Boots. And with banks being in a hurry to shift their risk, this may put further pressure on the market.

3. “The borrower is the servant to the lender” (Proverbs 22:7)

- There was an unusual bond issue last week from the Commissioners for the Church of England: £550m of 10- and 30- year bonds at Gilts + 120bp, backed by its £10bn endowment fund.

- The Church of England is rated by Moody’s as Aa1, ie more creditworthy than the UK Government (Aa3) but not as good as Microsoft (Aaa) which makes sense: of course the CofE less likely to default than this current UK government, but Bill Gates has more money than God.

- Despite the angelic credit rating, the CofE is paying 120bp more than the UK Govt to borrow – and more than Cambridge or Oxford Universities, although maybe this reflects that the two universities have been around for 800-1,000 years compared to the CofE’s mere 500 years.

- The bonds were of course Sustainability Linked – presumably there is a 40-day grace period?

- The bond’s Risk Factors included: safeguarding and reputational risks, failure of counterparties (like Peter), Pensions (uncontrolled longevity risk?).

- Final redemption is not optional and there is no parental guarantee.

- This story should be paired with 3i announcing that “3i invests in Christ” and news last December that “Christ secures 3-year debt extension”. Oh and apparently Jesus Holy Christ is a director of Weight A Minute Ltd, with occupation listed as Creator and Nationality as Angelic. Jesus H Christ was apparently born in 1971 which may lead to some more work for James Ussher.

Recent UK deals

- Whitbread signed a £775m 5+1+1 RCF with 7 banks including Santander, Bank of China, Barclays and NatWest, downsized slightly from its previous £850m deal.

- Halma signed a new £550m 5+1+1 RCF alongside a new £300m USPP (see below).

- Hg signed a £397m loan with Golub for its acquisition of Ideagen.

- Ocado signed a £300m secured RCF alongside £575m equity raising. The RCF ‘primed’ Ocado’s existing unsecured high yield bonds which were downgraded by Fitch.

- GCP Infrastructure increased its RCF to £190m from £165m, adding Mizuho to its group of RBSi, Lloyds, Allied Irish Bank and Clydesdale, paying SONIA +200bp.

- Ares provided c. £1bn to fund the MBO of Caretech, comprising an underwrite of £250m of super senior term loan and RCF to be syndicated to banks, £210m of long-term debt and £350m bridge to a disposal via sale & leaseback, followed by a portion of subordinated PIK notes (alongside Three Hills Capital) and a sliver of non-voting equity.

- Lookers extended £100m of 3-year revolving credit facility.

- Not a new deal but interesting nonetheless: The cinema chain Vue fell into the hands of its senior secured creditors. Value was assessed to fall within the senior secured loans, wiping its equity owners AIMCO and OMERS, and PIK lenders entirely.

USPP

- Dechra signed €150m of 7- and 10—year private placement facilities with an average coupon of 3.8% (so about mid-swaps +190bp).

- Halma issued £330m of private placements in GBP, EUR, USD and CHF with a 7-year average life.

- Segro issued 15- and 20-year EUR USPPs at 4.1% (equivalent to about UST+190bp).

Bonds

- Rentokil issued bonds to refinance its bridge for the acquisition of (Terminix: £400m 10-year (G+225bp), €850m 5-year (mid-swaps + 170bp) and €600m 8-year (mid-swaps +200bp). Sterling bonds were priced at 5.2% yield with the EUR at 4.2-4.6%.

- The AA issued £250m of 7-year sterling bonds to refinance a 2023 maturity at 7.375%, which was a new issue premium of around 75bp. The AA also launched and then cancelled a tender offer for its 2024 and 2025 bonds (which would have been funded by an upsize to the new deal). It is likely that it felt the pricing on the new issue was too much to pay to refinance bonds with maturities in 2 and 3 years. However, 3 weeks after launch, the bond is still yielding over 7%.

Our services

Numis is an ambitious, dynamic and innovative investment bank, driven to excel across all aspects of its delivery.