-

BackWhat we doNumis is an ambitious, dynamic and innovative investment bank, driven to excel across all aspects of its delivery.Investment Banking

-

BackLatest newsRead the latest news about our business, our people and our work, find out about our next events and conferences.News

-

BackWho we areOur collaborative environment and distinctive way of excelling , is nothing without our great people.

-

BackOur board

Numis at a glance

Our Articles

28

Mar 2024

31

Jan 2024

Latest Transactions

London Stock Exchange Group PLC

£1.4bn

Co-global coordinator on the £1.4 billion sell-down of the London Stock Exchange Group PLC

March 2024

Custodian Property Income REIT

£237m

Sole financial adviser, sponsor and corporate broker

January 2024

Numis On Twitter

Debt Advisory Update

As with many things, I’m a bit of a late adopter and this week I finally caught COVID. So far, it’s not so bad, perhaps because I’ve had both vaccinations. Although at some point between 8am and 10am yesterday, I lost my sense of taste and smell, which I’m finding really bizarre.

So I’m confined to my house / garden for next week, which is a shame as I was looking forward to seeing everyone at our new offices.

TL / DR: the cost of fallen angels, UK take-private financings, Islamic defaults

If you have time, this is an excellent and thought-provoking essay from BlackRock’s ex-CIO of Sustainable Investing, with a punchy intro: “My thinking evolved from evangelizing ‘sustainable investing’ for the world’s largest investment firm to decrying it as a dangerous placebo that harms the public interest”.

1. Fallen Angels and Rising Stars

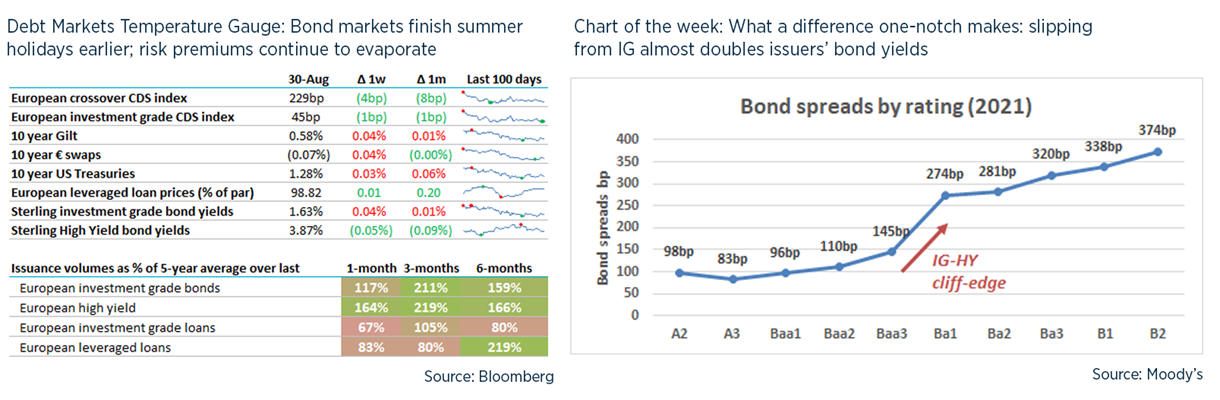

- As shown in the chart of the week, falling just one notch from investment grade (Baa3 / BBB-) dramatically increases borrowing costs (or investor return) – from 145bp to 274bp.

- Historically, many investors, particularly US regulated investors such as insurance companies or life funds, faced restrictions on sub-investment grade exposures – and even now, the NAIC and Solvency II rules can require much more capital to be allocated against non-investment grade exposures.

- Moody’s first started publishing ratings after the 1907 crash (also known as the “Knickerbocker Crash”, caused by a failed bank-financed attempt to corner the market of United Copper Company – the City really is less colourful now!). A leading bond text book from 1938 suggests the phrase “Investment Grade” was well-understood by then to mean Baa or better.

- There is often money to be made investing where others cannot go and many studies have found that HY bonds compare well against equity on risk-adjusted basis – particularly in the “fallen angel” territory of Ba. I can’t help but think this could be tougher now “high yield” yields are well below 4%.

- As the FT notes, blue-chip corporates often go to great lengths to preserve their IG rating, e.g. Tesco’s long journey back to IG through 2016 to 2019 via paused dividends, mergers, disposals and restructurings. Which is all in sharp contrast to private equity which celebrates leverage, as seen in part 2 below.

- One theory is that private equity benefits hugely from the ability (via limited liability) to threaten to walk away from bad investments – like all options, the value of this is increased by maximising volatility, i.e. less equity and more leverage. While lenders may price this in, there are other creditors who cannot e.g. employees, suppliers, landlords.

2. Take private financings

- As the Guardian and Daily Mail have spotted, there’s been a spate of private equity public-to-private deals, so here’s some takeaways from the deals.

- Leverage remains high – the senior debt packages for Sanne and Ultra are 6-7x 2022 consensus EBITDA (before including any pro forma adjustments). Yet despite this, debt margins are typically 325-425bp, as most of these deals are big enough to be syndicated to desperate institutional loan or HY investors.

- Widespread participation across banks, with perhaps Goldman Sachs and BNPP showing up more than most. Lloyds, Santander and NatWest less visible than Barclays and HSBC.

- JPM declined to be part of the Morrison’s financing, missing out of £20m of fees, despite being lead adviser – maybe it thinks this deal is not a good risk-reward. JPM is also missing out on Ultra, as it is advising on the sell-side.

- Limited showing by direct lenders – unlike last year, when many of the P2Ps were financed by credit funds, this year it is mostly banks. However, credit funds have invested in various parts of subordinated debt and PIK, at 7-10% yields.

- Deal by deal below (public sources, some numbers approximate).

- Sanne (Apax): $735m of senior and $180m second lien loans, provided by Bank of America and Deutsche Bank, plus some PIK notes sold to Carlyle. Excluding the PIK, leverage is about 8.6x 2022 consensus EBITDA – no doubt some PF / run-rate adjustments to be made to this …

- Ultra (Cobham / Advent): £1bn in $ / € secured loans from Barclays, CS, BNPP, HSBC, Jefferies, Morgan Stanley, RBC, Goldman Sachs and UniCredit with margin of L / E + 375bp. There is also $460m in subordinated debt privately placed with KKR, Goldman Sachs, Carlyle and Canyon Global Capital which pays 8.25%. Finally there is £315m of PIK notes with the same group of private lenders plus Albacore and Broad Street which pays 9.5%. Altogether, this is about 10x consensus EBITDA for 2022, although ‘only’ 6x at the senior secured level.

- NB Albacore had a similar role in take-private deals for EI Group and BCA in 2019.

- UDG (CD&R): $2.4bn senior secured loans in $ / € and £330m 2nd lien loan via Citi and JPM (and a host of junior bookrunners). This combined UDG with Huntsworth, acquired in March 2020. The banks were marketing it on 6.7x leverage but some investors said leverage was more like 7.5x if only some of the add-backs were permitted.

- Morrisons (CD&R): Goldman Sachs, BNP Paribas, Bank of America and Mizuho are leading £4.4bn of senior secured debt (of which over half expected to be in a sterling high yield bond and the rest in £ and € loans) and £1bn unsecured bonds in £ and €. Loans margins expected to be SONIA +400bp for the sterling and E+325bp for the EUR (although these will need to be swapped back to £). The secured and unsecured bonds expected at <4% and 5% respectively. This would be leverage of just under 5x consensus for 2022 though no doubt the arrangers will find some adjustments to bring this closer to 4x.

- Stock Spirits (CVC): £325m of term loans and €100m RCF, from ING and Citi’s Polish bank – ND / EBITDA about 4.25x.

- St Modwen (Blackstone): £1.15bn term loans from RBC, JPM and United Overseas Bank – LTV about 78%.

- Augean (Ancala / Fiera Instrastructure): £125m of secured loans from NatWest and Nomura, which is about 4x 2022 consensus EBITDA.

- John Laing (KKR): £550m facility from Goldman Sachs, Credit Agricole and BNP Paribas.

- Aggreko (TDR / I-Squared): $1bn secured term loan paying L+450bp with secured bonds of £1bn and unsecured bonds of £350m to follow, in € and $. This is led by Barclays, Bank of America, Deutsche Bank, Goldman Sachs and Santander.

3. Islamic defaults

- Earlier in June, the $500m 2023 bonds issued by Indonesia’s national flag carrier Garuda fell by 50%pts in a week as the airline declared that it would not be paying ‘interest’.

- It’s not really ‘Interest’ as sukuk / sharia-compliant financing doesn’t permit this; instead, sukuk bonds are often structured as complex JVs or sale & leaseback where ‘lenders’ actually have an ownership interest and ‘periodic distribution rights’ along with the right for the interests to be redeemed on a dissolution date at the end of the ‘bond’.

- Technically I think this makes a sukuk closer to a secured bond than anything else but this is all needed to show that the ‘lenders’ are actually entering into a commercial risk-seeking venture as opposed to just lending money.

- As a flavour, check out Garuda’s structure diagram on page 44 of the OM here; this discussion by some Denton lawyers is also revealing as they attempt to dance on the head of a pin.

- Earlier this year, the UK government issued its second sukuk bond, for £500m, by entering into a sale & leaseback for government offices. It finally priced in line with normal Gilts, which is an achievement considering it took 57 pages to explain the structure. Normally, secured debt has lower yield than unsecured debt but I suppose this is a UK government bond under UK law, so if they’re not going to pay you then no amount of collateral will help.

- The global market for sukuk issuance should top $200bn this year, led by the governments of Malaysia, Indonesia and Saudi Arabia, but the market is still developing some of the finer details, like how to enforce recovery upon default. Fitch wrote a note that sounds almost indecently excited that Garuda might shine a light on what actually happens when an Indonesian sukuk defaults.

- As one commenter wrote under the FT article on Garuda, “for it to be truly Islamic, there must be risk sharing. So it will always be quasi-equity”. The structuring resembles spending hours training a chicken to walk and quack like a duck – which is fine until it’s time to eat it.

UK Financings this week

- National Grid printed €850m 7-year green bond and 12-year “brown” bond. The green bond printed without any new issue premium, whereas the brown bond had about 7bp of premium vs existing bonds.

- Triple Point Social Housing REIT placed £195m of 10- and 15- year sustainability-linked noes with MetLife and Barings at 2.63%. The actual sustainability targets (if any) were not disclosed.

Our services

Numis is an ambitious, dynamic and innovative investment bank, driven to excel across all aspects of its delivery.