-

BackWhat we doNumis is an ambitious, dynamic and innovative investment bank, driven to excel across all aspects of its delivery.Investment Banking

-

BackLatest newsRead the latest news about our business, our people and our work, find out about our next events and conferences.News

-

BackWho we areOur collaborative environment and distinctive way of excelling , is nothing without our great people.

-

BackOur board

Numis at a glance

Our Articles

28

Mar 2024

31

Jan 2024

Latest Transactions

London Stock Exchange Group PLC

£1.4bn

Co-global coordinator on the £1.4 billion sell-down of the London Stock Exchange Group PLC

March 2024

Custodian Property Income REIT

£237m

Sole financial adviser, sponsor and corporate broker

January 2024

Numis On Twitter

Debt Advisory Weekly

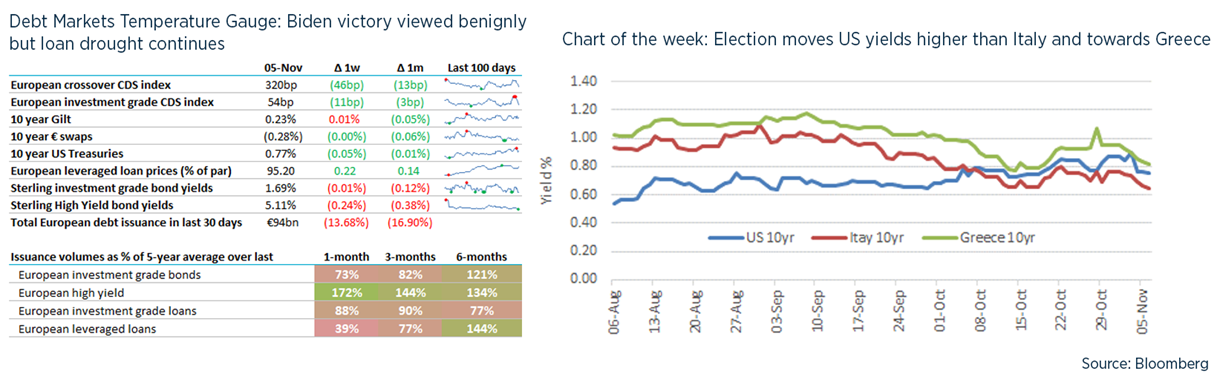

This is only a brief one so that we can all get back to refreshing our screens to see if Biden’s vote tally has changed yet.

TL / DR: New leverage for private equity; pulling the ION out of the fire; Record order book for EZ

1. Private equity finds new ways to add leverage

- When I worked (briefly!) in private equity, I was once given a sales pitch by a bank that offered to (a) leverage the operating asset, (b) leverage the equity position (NAV lending) and (c) lend to me to facilitate my personal investment into the fund. If the meeting had continued for much longer then I think they would have also offered my kids a credit card each.

- NAV lending is against a portfolio of private equity assets, at a LTV of maybe up to 40% of the equity value. There are obvious benefits to the private equity sponsor – it may accelerate distributions to LPs that could trigger paying carried interest to the sponsor. Investec and Deutsche Bank are big players.

- Covid-19 has led to an explosion of interest in NAV lending – some of which has not yet been disclosed to fund LPs: PE firms are choosing to leverage the equity position to deploy more capital to fix liquidity / solvency problems in portfolio assets, rather than call for more equity from LPs. The FT wrote about it here.

- The rationale might be as simple as the fund being beyond its investment period, or bridging a temporary liquidity shortfall that doesn’t merit permanent equity; but it could also be one last roll of the dice before confessing to the scale of the problems to end-investors.

- My sense is that it’s like any leverage: great when going well but could be a real problem if problems persist, particularly if not disclosed to LPs in advance. Typically, the last assets in a PE fund are the hardest to sell, and for good reasons …

- Incidentally, while researching this, I came across an entirely new form of leverage: “management fee swap” – more here (p53). Investec wins this week’s competition for most innovative debt product.

2. Keeping your ION the ball

- In keeping with last week’s discussion of direct lending, I noted that ION had financed its acquisition of Acuris (i.e. MergerMarket and Debtwire) via a $1.25bn unitranche with HPS and Goldman Sachs. This had 3% up-front fees and margins of L+775bp.

- ION Analytics had launched a deal las week via Credit Suisse and UBS to refinance this with syndicated leverage loans, at E / L+425bp. Even taking into account a hefty prepayment penalty for the unitranche lenders, this would have saved them money within 12 months.

- But the deal was cancelled this week; the bookrunners blamed the election (were they surprised it was happening this week??) but investors cited aggressive structuring, in particular some very imaginative EBITDA adjustments, as well as too skinny pricing.

- This could be seen as just unfortunate except that UBS had a very similar experience last year with ION Corporates’ deal that was aborted twice last year for similar reasons (more here).

- Takeaway: deals are structured around what works for a borrower but they also need to anticipate how a deal looks from the investors’ perspective.

3. EZ does it

- The EU recently set a record order book for a deal: €150bn of orders for a €17bn financing for its SURE bond programme to yield -0.24% (-ve).

- Investors loved the rating (AAA) size (great liquidity), yield (35bp pick-up v German debt) and ESG flavour.

- Showing that bankers have no monopoly on clunky acronyms, this is named after the Support to mitigate Unemployment Risks in an Emergency (do you see what they did there?). More here.

- For me this is mostly interesting as it seems like a concrete step towards fiscal integration: federal programmes (and government debt, and the US$) keep the US more or less a single nation. The EU needs something similar to become an optimal currency area and become more robust to external shocks.

UK debt financings this week:

- Aston Martin Lagonda priced its 1st ranking high yield bonds last week at 10.5%, after abandoning the £ tranche and adding call protection out to 4 years. Now priced at 102.

- Morgan Sindall added 1 year to its £150m RCF to push to May-23 – expect a lot more of this.

- Pantheon International Participations (PIP) has amended and extended its £300m RCF, with £75m continuing to mature in Jun-22 and the reminder in May-24. It seems not all the lenders wanted the extension.

- Ports of Jersey has signed a debut £40 RCF.

Our services

Numis is an ambitious, dynamic and innovative investment bank, driven to excel across all aspects of its delivery.