-

BackWhat we doNumis is an ambitious, dynamic and innovative investment bank, driven to excel across all aspects of its delivery.Investment Banking

-

BackLatest newsRead the latest news about our business, our people and our work, find out about our next events and conferences.News

-

BackWho we areOur collaborative environment and distinctive way of excelling , is nothing without our great people.

-

BackOur board

Numis at a glance

Our Articles

28

Mar 2024

31

Jan 2024

Latest Transactions

London Stock Exchange Group PLC

£1.4bn

Co-global coordinator on the £1.4 billion sell-down of the London Stock Exchange Group PLC

March 2024

Custodian Property Income REIT

£237m

Sole financial adviser, sponsor and corporate broker

January 2024

Numis On Twitter

Debt Advisory Weekly

Another week, another vaccine. If you’re missing the excitement of watching Biden’s votes creep up, this is a slightly slower version showing progress of all potential vaccines in real-time.

TL / DR: Fictitious EBITDA; More waivers and back to 10% placings; the Crown Preference

1. A Bridge Too Far

- Moody’s was out this week with its analysis of EBITDA adjustments – how much issuers (particularly PE-backed) massage their leverage with add-backs to EBITDA e.g.

- Boparan this week successfully refinanced with £475m of HY at 7.625%– something which looked unlikely 12 months ago but they have been rescued by the disposal of Fox’s biscuits.

- Marketing “pro forma adjusted run rate EBITDA” was £135m, but some investors identified ‘actual’ EBITDA at £100m after removing the effects of an extra week in 2020, contribution from disposed businesses and adding back some COVID-related costs (but not the benefits of COVID from more eating at home).

- Leverage was 3.3x (marketing) / >5x with ‘actual EBITDA / >7x with pension deficit. This stress led it to price at Gilts + 761bp, exactly in line with PureGym last week.

- Moody’s believes that 2019 saw ‘peak adjustment’ to EBITDA with actual leverage for the average new issuers being close to 7x vs marketing leverage of just over 5x.

- They also check whether issuers achieve all the run rate / pro forma adjustments: in 2019, it believes that about 1/3 of the 2018 issuers fell short of the promised EBITDA adjustments.

- It’s always been a bit of an anomaly that leveraged borrowers try to spoof institutional lenders with so many adjustments whereas normal corporates can’t get away with this with their banks. One reason is possibly that LBOs are more typically mid-transition than ‘normal’ corporates – maybe Covid could be the catalyst where all borrowers get to adjust their EBITDA as they muddle through – also known as EBITDAC.

2. 2021: Rinse & repeat

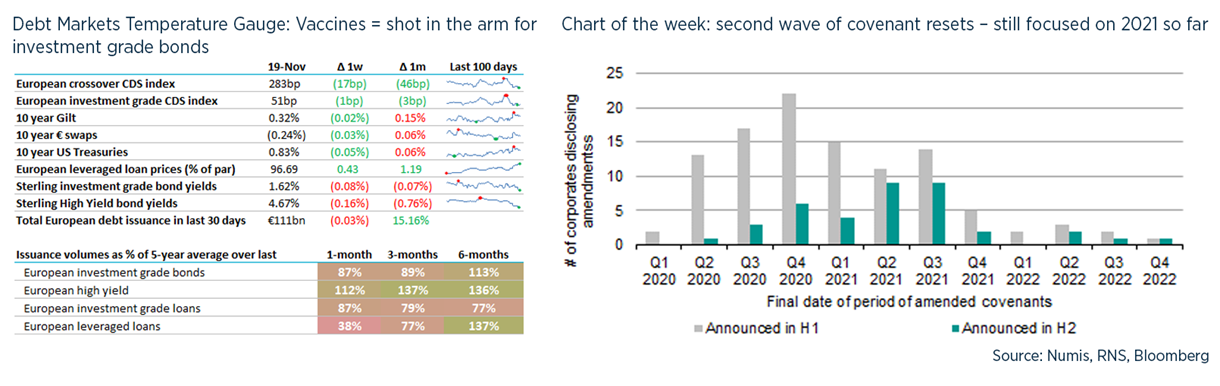

- We spent much of Q2 and Q3 helping borrowers achieve more covenant and liquidity headroom – we tracked over 150 borrowers that on average waived or amended covenants out to Q2 2021.

- Given Covid is not yet cured and that most of us are still in lockdown 2.0, there have already been many borrowers needing to extend this forebearance e.g. Stagecoach has come back for a second bite of the cherry after getting waivers in June, as has Marston’s.

- So far, this second waive of covenants is still focused on H2 2021 though some are stretching into 2022, particularly where this is alongside an equity raising.

- We are seeing a wave of borrowers seeking new waivers to ensure their going concern is not in doubt for their accounts at Dec-20 – some will be easy, others will be more difficult if their business model has been permanently damaged by C19 (even if the vaccine works) or if the disruption of 2020 has led to unsustainable debt levels.

- In this context, the news today that limit for non-pre-emptive equity placings will be reduced back to 10% has the potential to cause a backlog if lenders demand >10% equity to remediate overleveraged borrowers – rights issues take much longer and are more expensive.

3. The Crown Preference

- This came up in conversation with a colleague this week – how many ways can debt be subordinated? This isn’t normally a thing for listed shares, since “equity” has its roots in “equal”. Founder shares are still relatively uncommon in the UK and preference shares are really something quite different.

- The obvious ways are collateral (secured vs unsecured) and contractual (simply agreeing to repaid at the end in liquidation). The other more common way is structural (lend to a shareholder of an operating company).

- More nebulous is “temporal subordination”: agreeing to be paid back at a later point in time than other (otherwise equally ranking) shareholders.

There is a final form, which is about to get a bit more controversial in the UK: statutory subordination. The UK Govt has decreed the return of the Crown Preference. HMRC will move from an unsecured creditor to ranking ahead of floating charges (in respect of NIC, PAYE, and VAT but not Corporation Tax). - This may have a big impact on inventory financiers and will generally dilute returns for unsecured creditors. But the alternative is that the public purse effectively subsidises specialist financing firms (and by extension, SMEs).

UK debt financings this week:

- Drax has agreed a new 5-year £300m RCF linked to an ESG and its carbon intensity levels. This marks the completion of a busy period for Drax where it has also entered into £160m 10-year infrastructure loan agreements and issued €250mn of EUR high yield.

- Assura has reduced their RCF to £225m (by £75m) ahead of the requirement to do so in May-21 and has also repaid a £100m secured bond – this follows its social bond in February.

- Diploma has completed the syndication of the £271m equivalent loans backing its acquisition of Windy City Wire; the financing includes a $170m TL and £135m RCF.

- Intact Financial Corp has announced that it will be backing its £7.2bn joint acquisition (with Tryg) of RSA with £1.815bn of loans from Barclays and CIBC.

- Boparan priced £475m of 5NC2 sterling high yield bonds at 7.625%, in line with guidance.

- National Express priced an inaugural £500m hybrid bond (rated BB+/ Ba1) – this will be treated as 50% equity by the ratings agencies, which should improve credit metrics as it replaces other debt. This priced at 4.25%, significantly tighter than the 5% area guidance. It is perpetual but expected to be refinanced in 5.25 years. It’s about 250bp wider than its vanilla corporate bonds.

Our services

Numis is an ambitious, dynamic and innovative investment bank, driven to excel across all aspects of its delivery.