-

BackWhat we doNumis is an ambitious, dynamic and innovative investment bank, driven to excel across all aspects of its delivery.Investment Banking

-

BackLatest newsRead the latest news about our business, our people and our work, find out about our next events and conferences.News

-

BackWho we areOur collaborative environment and distinctive way of excelling , is nothing without our great people.

-

BackOur board

Numis at a glance

Our Articles

28

Mar 2024

31

Jan 2024

Latest Transactions

London Stock Exchange Group PLC

£1.4bn

Co-global coordinator on the £1.4 billion sell-down of the London Stock Exchange Group PLC

March 2024

Custodian Property Income REIT

£237m

Sole financial adviser, sponsor and corporate broker

January 2024

Numis On Twitter

Debt Advisory Weekly

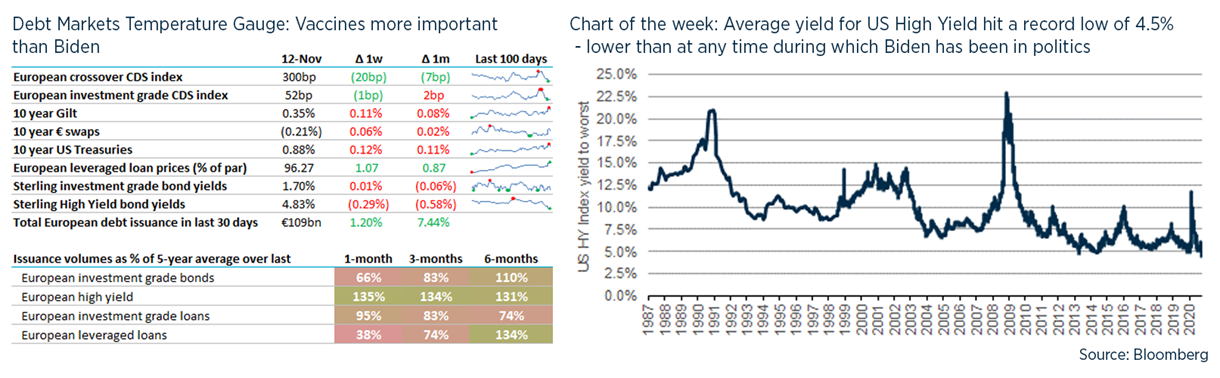

Now that we’ve ‘got’ a vaccine, markets have reacted like it will all be over by Christmas. Hopefully the US election result will be certified sooner than that, though Nevada is doing its best to drag it out.

TL / DR: UK high yield on fire; Green Gilts = Grilts?; Extended govt support

1. UK High Yield on Fire

- Some good news for leveraged UK borrowers this week with a slew of new HY issues that timed the market to perfection – all of which priced tighter than initially marketed (“price talk” or “whispers”, which is not as exciting as it sounds): PureGym, M&S, Travis Perkins, Cabot, Thames Water. All these deals have traded up in secondary. Some interesting takeaways for other issuers:

- Closed for business ≠ closed to markets: PureGym’s lending bankers have been sitting on a €445m acquisition bridge since December last year and launched on Monday just 2 hours before the vaccine news broke. Having marketed the deal initially with a yield as wide as 9.6%, it eventually priced at 6.9% (not a number transposition error). Order book of 3x.

- Fallen Angels still have a halo: M&S is now firmly ‘junk’ (Ba1 / BB) but priced a new 5.5 yr £300m deal at 3.75%, at G+363bp on investment grade-style documentation. Order book 7x.

- Deteriorating credit ≠ high debt costs: Travis Perkins priced a “five Bs” (BBB- / BB+) £250m 5.25 yr deal at 3.75%, which is its lowest ever coupon. This is all down to Gilts though since its spread was 40bp higher this time around.

- Shop around for credit ratings: PureGym dropped S&P as a rating agency in September, which at CCC+ had a lower rating than Moody’s and Fitch. Travis Perkins added Fitch in October, which has a better rating (BBB-) than S&P (BB+).

- Credit ratings are important but there is more to pricing: All of M&S, TP, Cabot and Thames Water all had a BB+ rating from at least one agency. But issuance yields varied from 3.75% to 5.375%.

2. Grilts

- In a bid for good headlines and improve his leadership chances move to enhance the environmental credentials of the UK government and improve the social purpose of capital markets, Rishi Sunak this week announced that the UK will issue its first Sovereign Green Bond next year.

- These are “green” in that the proceeds are somehow to be allocated towards projects that “will tackle climate change, finance much-needed infrastructure investment and create green jobs”.

- I didn’t see that the HMT announced any new projects nor is it clear how we can be sure the proceeds are specifically directed towards greenness. This interview suggests that it will be down to “just the trust in the government”, which has worked so well elsewhere.

- It’s always worth noting that the “greenium” by which green bonds have a higher price (lower yield) than normal bonds is a bit elusive e.g. one Stanford study found the greenium was “essentially zero”.

- But if there really were a greenium then it would imply that non-green financing should yield slightly more for having separated out the “green use of proceeds”. Additionally, the UK’s Debt Management Office worries that creating Grilts will fragment the Gilt market and reduce liquidity and drive up borrowing costs overall.

- All of this is just an excuse to link to my favourite financial innovation from Denmark’s central bank: a ‘Green Certificate’ which is a “zero coupon bond with zero redemption at maturity”.

3. The British Business Bank – like TSB, the bank that likes to say “yes”

- (incidentally, while finding those links, I was amazed to find the TSB produced a monthly music magazine for its younger customers called “TS Beat” – banking really did used to be more fun).

- Possibly the only upside to “Lockdown – The Sequel” is that the government support schemes have been extended, not just furlough but also the loan guarantee schemes from the British Business Bank.

- The CLBILS and CBILS will now be open for new applications until to 31 January 2021.

- When data was last available, banks were processing 19,000 Bounce Back Loans each week – but only 262 CLBILS and 14 CLBILS deals, which frankly feels like taking a knife to a gunfight (remembering Sean Connery here). More data expected this week.

- End of year / going concern preparation is now driving a number of discussions that we are having with clients and their banks about next year’s covenants and loan maturities in 2022 – it feels like there will be a lot to do in Q1 2021 and we expect these schemes to be in more demand and extended again.

UK debt financings this week:

- Smith News has extended its £120m 3-year facility by 2.5 years, with its margin increasing by 300bp – along with new amortisation and prohibition on dividends.

- FirstGroup has amended covenants on its banking facilities and PPs up to Sept-21, increasing their leverage to 4.5x-5.5x and interest cover ratio to 1.4x in the meantime.

- Whereas Informa has cancelled a £750m 18-month credit facility, alongside its PP loans removing all financial covenants.

- Target Healthcare REIT has increased its existing bank facilities to £80m and £70m (from a total of £130m) and switched to SONIA, with NatWest and HSBC.

- Cabot, Travis Perkins, PureGym, Thames Water and M&S sold HY bonds as above.

- International Personal Finance last week completed an exchange offer for its 2021 € notes, completing a new deal at a yield of 10%; this has subsequently traded down to bid yield 10.8%.

- Marston’s launched another consent process for the financial covenants in its securitisation, offering a 5bp fee, which looks like a good deal when Unique (Enterprise Inns) paid 75bp earlier this year.

Our services

Numis is an ambitious, dynamic and innovative investment bank, driven to excel across all aspects of its delivery.