-

BackWhat we doNumis is an ambitious, dynamic and innovative investment bank, driven to excel across all aspects of its delivery.Investment Banking

-

BackLatest newsRead the latest news about our business, our people and our work, find out about our next events and conferences.News

-

BackWho we areOur collaborative environment and distinctive way of excelling , is nothing without our great people.

-

BackOur board

Numis at a glance

Our Articles

28

Mar 2024

31

Jan 2024

Latest Transactions

London Stock Exchange Group PLC

£1.4bn

Co-global coordinator on the £1.4 billion sell-down of the London Stock Exchange Group PLC

March 2024

Custodian Property Income REIT

£237m

Sole financial adviser, sponsor and corporate broker

January 2024

Numis On Twitter

Debt Advisory Update

Following a short break while I was battling the winds in Cornwall, see below our weekly debt discourse.

TL / DR: Victoria’s Red Carpet; CCF Facility – Dismissed!; Direct lending pulls up short

1. Victoria’s Red Carpet

- This mailout isn’t supposed to be an (obvious) advert for our work but we were delighted to have advised Victoria on Koch’s £175m investment via perpetual convertible preferred equity (RNS here).

- It’s a fascinating deal but quite complex with new preferred equity, secondary equity and a share buyback so just ask us if you’d like to get full details.

- The highlight is that we structured the deal so that Victoria’s credit ratings were unaffected, with Moody’s and Fitch treating the investment as equity.

- Preferred equity investments are relatively common in the US (see here or here) but we believe that this is unique for a UK-listed company with public credit ratings.

- The pref has a coupon of 9-10% plus warrants for 9% of the equity at 20% discount to current share price. However, Victoria assessed this all-in cost against issuing equity at a price which was 60% down from its 2018 peak (and which has risen.

- Shareholders (+24%) and bondholders (+2 pts) both liked the deal.

- We have great relationships with several very keen investors who are on the lookout for opportunities to deploy hybrid / non-control capital – we are progressing another similar situation now but we’ve always capacity for other deals.

2. BoE’s Covid Corporate Financing Facility gets tougher

- Last time, we looked at the BoE survey of banks’ credit officers but forgot to mention that the Old Lady has herself been tightening up on credit criteria.

- Back in April and May, we checked the BoE webpage for the Covid Corporate Financing Facility (CCFF) every morning, trying to work out what had changed overnight.

- Now a major revision of the rules was announced on 9 October and so far as we can see there was nothing in the FT and only a cursory article in Bloomberg / Reuters.

- [change is that now issuers must be investment grade today and not just pre-C19].

- In truth, the lack of news tells its own story: CCFF was useful for about 1 month when short-term commercial paper markets looked like they might fail, which prompted issuers to draw down their backstop RCF lines. However, bond markets provided all the liquidity investment grade borrowers could ever want.

- So the CCFF became the playground of fallen angels (e.g. SSP, RR) which had lost their IG rating and global multinationals looking to arbitrage funding markets (looking at you BASF and Baker Hughes).

- The Bank of England does not like taking credit risk directly and instead prefers that banks face the flack for poor credit decisions – hence why CLBILS is being extended.

- But even so, the CLBILS scheme is hardly a runaway success: recently this scheme has seen just 10-20 loans approved each week for an average of £5-7m per loan.

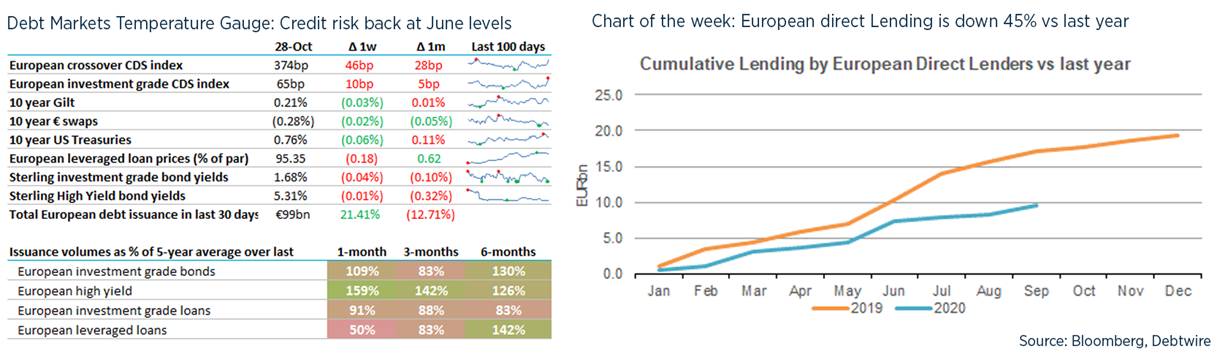

3. Direct lending throws away its shot?

- C19 disruption was supposed to enable direct lenders to pick up share but the recovery in the HY market pushed them back to their traditional heartlands of the UK mid-market (stats here)

- Additionally, direct lenders have often become indirect owners where existing borrowers have been hit hard and equity has been wiped out. We are working on a deal like this now and it’s likely to end painfully for the lender.

- As with everything, the direct lending market faces a “K” shaped recovery (more here): good assets are being chased by direct lenders who are conceding pre-COVID terms; but business impacted by C19 are struggling to get traction.

- The HY market is more willing to put a price on this risk though let’s see if this week’s Aston Martin HY deal roars away or crashes, in a difficult market.

- While there are the occasional outsize deals like ICG’s €600m unitranche for Funecap or Ares lending £1bn to Daisy, direct lending remains focused on mid-market deals or those that are too difficult for the syndicated loan / HY markets e.g. Ardonagh and Acuris.

- This will change, not least because the big direct lenders are raising so much that they need the €500m+ deals to move the needle e.g. Apollo’s partnership with Mubadala that will only look at deals of $1bn+. But whether these prove to be good investments …

UK debt financings this week:

- Aston Martin’s lenders have agreed to extend £87m of RCF commitments alongside its new equity raise and HY bond issues. £840m eq of high yield are being sold this week, indicated at 8-9% but let’s see. £259m of subordinated notes were priced at 13.5% coupon plus warrants over 5% of the company (if this are nil-cost warrants then I think these sub notes have return of >20% at the current share price).

- Manchester United has agreed a new secured £50m RCF maturing in 5 years at L+250bp and Greencoat Renewables has agreed a new €200m 5 year TL.

- C&C Group has extended its waivers until Aug-21 and replaced with a minimum liquidity covenant of €150m at month end (aside from Dec-20).

- Savills has refinanced two Italian assets with a green loan.

- Getlink (née Eurotunnel) priced €700m 5NC2 green high yield at 3.50%.

- Lowell Financial priced £1.6bn-equivalent senior secured notes, with a €740m 2025 tranche paying 6.75%, a £400m 2025 note at 7.75% and a €600m 2026 FRN at E+625bps with a 98.5 OID – but it took £600m of fresh equity from Permira to get this away.

- Drax priced a €250m senior secured 5NC2 note at par, paying 2.625%.

Our services

Numis is an ambitious, dynamic and innovative investment bank, driven to excel across all aspects of its delivery.