-

BackWhat we doNumis is an ambitious, dynamic and innovative investment bank, driven to excel across all aspects of its delivery.Investment Banking

-

BackLatest newsRead the latest news about our business, our people and our work, find out about our next events and conferences.News

-

BackWho we areOur collaborative environment and distinctive way of excelling , is nothing without our great people.

-

BackOur board

Numis at a glance

Our Articles

28

Mar 2024

31

Jan 2024

Latest Transactions

London Stock Exchange Group PLC

£1.4bn

Co-global coordinator on the £1.4 billion sell-down of the London Stock Exchange Group PLC

March 2024

Custodian Property Income REIT

£237m

Sole financial adviser, sponsor and corporate broker

January 2024

Numis On Twitter

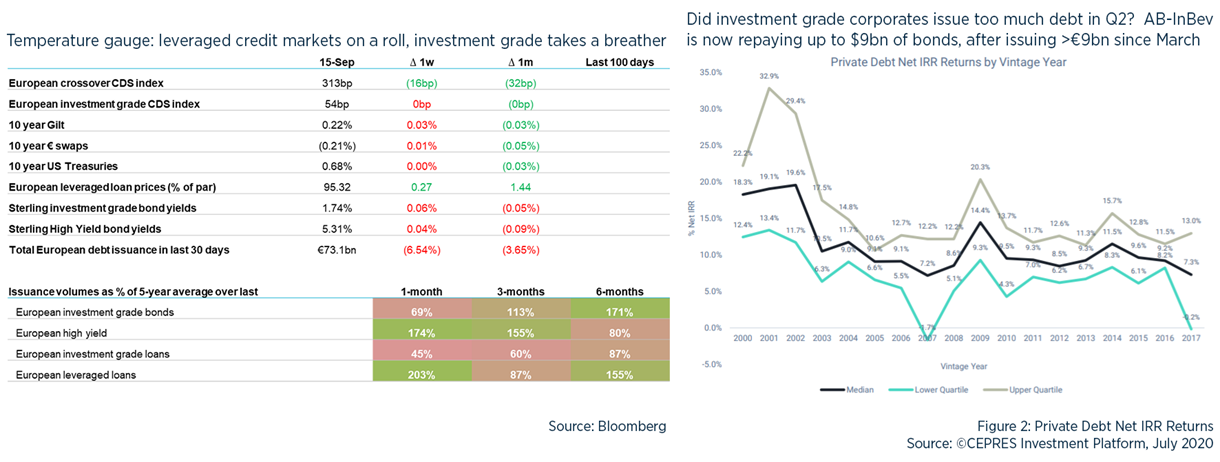

Debt Advisory Update

We’re pleased to publish our regular “specific and limited” weekly note about debt.

The end of Govt loan guarantees is nigh; UK corporates borrowing sustainably; Supply Chain Finance brought into the open

Killing BILS

- The Government’s guaranteed “Business Interruption Loan Schemes” for COVID-hit corporates will stop accepting new applications in 2 weeks.

- As of mid-August, total loans under CLBILS / CBILS were £13.7bn to 60,500 SMEs and £3.5bn to 516 larger borrowers (average loan of £6.8m)

- There are plenty of advisers to SMEs touting the schemes as a source of ‘effectively free cash’ since interest and fees are covered by the govt for the first year.

Not everyone has made their involvement public (possibly to avoid a backlash) but we have counted 23 UK-listed borrowers disclosing CLBILS loans totalling £0.5bn. The largest of these were for Restaurant Group and N Brown, who both drew down £50m, with JD Wetherspoon not far behind. - Was it a success? Let’s see when / if all these loans are repaid. But certainly for bigger corporates, our experience was that it was relatively unusual for CLBILS to generate much incremental bank appetite. Some lenders privately told me that they had suggested that borrowers avoid using the schemes if they could possibly do so, since there could be consequences in the future from having “taken government money” – as was seen in the revised rules for the Bank of England’s CP programme, which then prohibited dividends / bonuses for borrower.

- It will take time for the dust to settle and for the economists (apply here if you want) to come up with detailed analysis of the long-term impact. My sense is that the BILS schemes will have had a bigger impact than the CCFF CP programme but less than the furlough scheme. £17bn is still outstanding under CCFF – but of this over 40% has been drawn by corporates that don’t obviously deserve UK government support (BASF with its A rating …).

Borrowing sustainably

- Burberry this week priced another sterling “sustainable” deal: a debut bond for 5-year £300m at 1.125% (spread of 135bp to Gilts). Despite only having one credit rating, which is pretty unusual for a general corporate, this received over £2bn of orders and let the pricing tighten by 0.45% from initial guidance. Burberry promises to abide by its own Sustainability Framework which has received a blessing from Sustainalytics as being sufficiently demanding and robust. Key items include sourcing, environmental impact and communities.

- It is not yet known whether the Burberry deal features a MAC.

- Assura last week priced a 10-year Social Bond for £300m at 1.5% (spread of 128bp to Gilts), again promising to abide by a Social Framework again focused mainly on environmental and community impact.

- Overall, ESG bonds represented c. 4% of the market in Q1, up from 2.78%. Google issued $5.75bn and Germany €6bn of ESG bonds – and the European Commission is also looking at getting into the market.

- I’ve changed my views over the past year: ESG is becoming no longer just a “nice to have” for CFOs and Treasurers looking to polish their CV, but instead is something that all companies should consider before they launch an important financing, whether loans or bonds.

Reversing Reverse Factoring

- Like Moody’s, I’ve never been a fan of “reverse factoring” i.e. using a bank to intermediate between a company and its suppliers, stretching creditor days to boost cash flow.

- Banks like it because, from a regulatory perspective, it’s only a short-dated commitment so is relatively low capital for them. But this is exactly the problem for borrowers: entering into these arrangements concentrates a short-term credit decision from a multiplicity of suppliers to a single bank – possibly depending upon a single individual’s credit judgement.

- The main advantage of “supplier finance” was that it was disclosed only as additional “trade creditors” rather than financial debt, and so enabled Carillion to flatter its balance sheet. Vodafone has also used this technique in some quite creative ways.

- The IFRS has inched further along the path of requiring these arrangements to be treated as financing rather than operating - more discussion here. It seems to me that they may well reach a decision in a few years, long after this has ceased to be a major disclosure issue – since analysts / shareholders are moving significantly faster. My money is on the SEC to move fastest – as seen by its recent letters to Boeing and Coca-Cola looking for more info.

- I recall the first time I was told that finance lease / operating lease distinction would probably be shortly abolished: when I was training as an accountant in 1997. IFRS16 came into force properly this year.

Notable UK financings this week

- West Kent Housing secured £110m of new loans from NatWest to help form part of NatWest’s commitment to provide £3bn of new funding to the housing association sector over the next 3 years; Avon Rubber is backing its $130m acquisition of Team Wendy with a new 3-year $200m RCF; Drax has signed £160m equivalent of new infrastructure term loans in 4,6,7 and 10 year tranches.

- RCF repayments: Dunelm, Polypipe and Saga (after raising £150m in equity). Polypipe also repaid £100m that it had borrowed on the BoE CCFF.

Our services

Numis is an ambitious, dynamic and innovative investment bank, driven to excel across all aspects of its delivery.