-

BackWhat we doNumis is an ambitious, dynamic and innovative investment bank, driven to excel across all aspects of its delivery.Investment Banking

-

BackLatest newsRead the latest news about our business, our people and our work, find out about our next events and conferences.News

-

BackWho we areOur collaborative environment and distinctive way of excelling , is nothing without our great people.

-

BackOur board

Numis at a glance

Our Articles

28

Mar 2024

31

Jan 2024

Latest Transactions

London Stock Exchange Group PLC

£1.4bn

Co-global coordinator on the £1.4 billion sell-down of the London Stock Exchange Group PLC

March 2024

Custodian Property Income REIT

£237m

Sole financial adviser, sponsor and corporate broker

January 2024

Numis On Twitter

Debt Advisory Update

So, 2021 is just one week old and it looks like being another classic year. Well done to all those who have maintained “dry January” so far.

TL / DR: Groundhog Year; ESG gains market share; Bitcoin

1. Themes for the near year, same as the old?

- Covenant waivers: we are in discussions with several borrowers looking to extend / repeat their waivers, often for going concern sign-off. Some corporates have already announced new waivers, (IHG, The Gym Group, Marston’s) and others will follow with their results. I think it’s now reasonable to aim at waiving / amending all the way out to Dec-22 if the plan stacks up.

- Additional liquidity facilities: Despite Arsenal joining the CCFF team this week, more debt is not Plan A for most of our clients or their banks. Interestingly, we are seeing more corporates look at debt funds as being an alternative to equity when ‘normal’ debt is not available.

- Strong bond markets: European investment grade corporate bond volumes this week are only a little behind the start of 2020. It’s unlikely 2021 will match last year’s boom.

- Strong leveraged finance markets: HY and leveraged loan markets have been relatively quiet this week, with a punchy €3bn loan / bond deal for Verisure launching next week.

- Debt funds: a strong finish demonstrated by Ares reupping its commitments to Daisy Group by backing the split of DWS that brought in Inflexion as investor, as well as providing a £527m PIK at 13% for the TalkTalk take-private. Pemberton announced this week another $2.2bn for its European direct lending platform.

- Government funding: so far, no new direct funding schemes for anything other than the smallest companies, though the British Airways’ £2bn govt-backed ECA financing is one of the biggest ever for a corporate (i.e. not for a specific project or export).

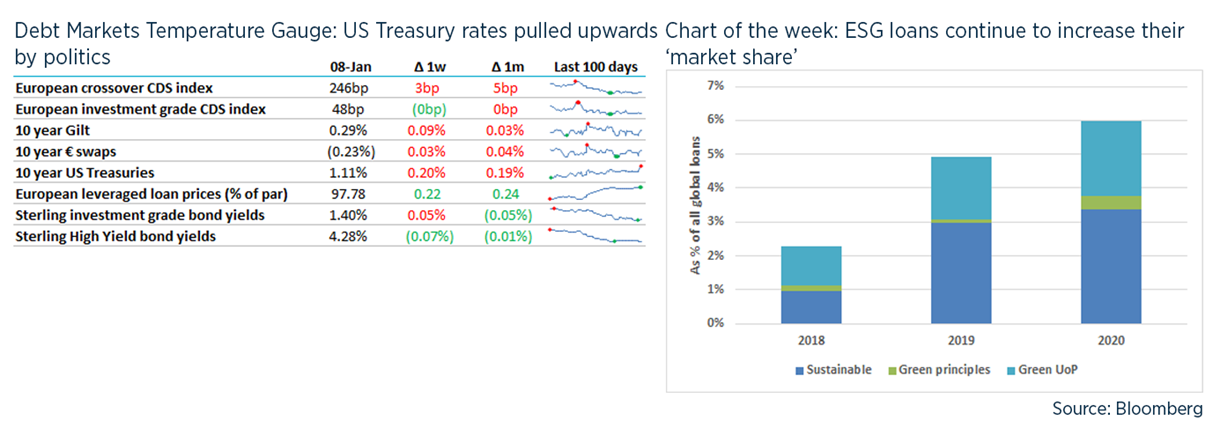

2. ESG driving lenders

- I’ve been a bit cynical about ESG lending for a while – some lenders have had more governance problems than even the dodgiest AIM-listed miner: HSBC’s Mexican money-laundering problems, Jes Staley’s witchhunt for a whistleblower (even after he’d been told not to do it), Deutsche Bank generally.

- The importance of ESG for equity investors seems to be driven by two factors:

- Shareholders controls the corporation and profit from its success, more so than lenders, and so shareholders are better able to change companies’ behaviour – and ‘more responsible’ when they fail to do so.

- lenders are for the most part acting as principals for their loans: the funds ‘belong’ to the bank; whereas most fund managers act as fiduciaries. This is tied up with Matt Levine’s theory that banks are socialist collectives, run for the benefit of their employees not shareholders.

- Adding a “ESG wrapper” will definitely improve a loan’s attraction to banks – but always provided the credit and returns already stack up: ESG is an overlay and the risk / reward has to make sense without it.

- E.g. SocGen recently announced cutting its exposure to Oil & Gas and tried to sell a $1bn portfolio of O&G loans – but halted the sale when bids came in too low.

- It’s easy for banks to turn their backs on Oil & Gas sectors (and cite ESG) when the sector’s in the doldrums – but will they continue to turn away if oil prices get back to $70+?.

- 23 banks signed into INEOS’s loans for the acquisition of further legacy BP businesses.

3. Bitcoin = what exactly?

- I’ve not commented on Bitcoin before as frankly I have viewed it as neither money nor an investment. But after I wrote about tally sticks Modern Monetary Theory recently, I thought this might be a good counterpoint – since Bitcoin is explicitly about not being deliverable as payment for taxes.

- Plus I finally got round to listening to this Bloomberg podcast titled “what turned Tracy into a Bitcoin bull?”.

- Startlingly, one of the Bitcoin evangelists on the podcast suggests corporate treasurers should invest some of their liquidity into bitcoin, because “it diversifies your risk and offers improves returns”.

- I know a good few treasurers but I don’t believe even the most racy would consider taking this to the board – but as there are so many Bitcoin bulls around, I’m happy to be told otherwise.

- I continue to be sceptical about Bitcoin: it’s not “money”, because by design it doesn’t have the force of any law or government backing; it’s not a store of value, because it’s so volatile and its convertibility into something useful remains at the whim of other speculators. But conversely, it’s not an investment, as it doesn’t entitle you to any real-world asset (or a derivative of a real-world asset).

- It seems that the only ‘asset’ that Bitcoin entitles you is ‘ownership’ of a (only relatively) unique identifier that you can sell to other people.

- So by all means feel free to ‘buy’ it if you think you are not the greater fool but it seems very like the “art market” without the aesthetic benefits.

- So far, as every purported benefit to bitcoin is refuted, someone comes up with a new one. It seems more like an ingenious solution in search of a problem.

UK debt financing:

- AstraZeneca arranged a $17.5bn bridge loan for its $39bn acquisition of Alexion Pharma, from Morgan Stanley, JP Morgan and Goldman Sachs, 12+6+6m.

- Virgin Media finalised a £1.5bn term loan for its merger with O2 at L+275bp with 29 banks (can you name 29 banks??).

- Stenprop arranged £66.5m 7-year fixed rate loan from ReAssure (part of Phoenix) at G+130bp (1.66%).

- Arsenal Football Club has borrowed £120m on the CCFF scheme to mitigate revenue losses, repayable in May 2021.

- Greggs signed a new 3-year £100m RCF to replace their CCFF borrowings.

- British Airways has signed a 5-year £2bn loan partially guaranteed by the UK Export Finance.

- Hipgnosis increased its RCF by $200m to $600m as it buys up the world’s song rights.

Our services

Numis is an ambitious, dynamic and innovative investment bank, driven to excel across all aspects of its delivery.