-

BackWhat we doNumis is an ambitious, dynamic and innovative investment bank, driven to excel across all aspects of its delivery.Investment Banking

-

BackLatest newsRead the latest news about our business, our people and our work, find out about our next events and conferences.News

-

BackWho we areOur collaborative environment and distinctive way of excelling , is nothing without our great people.

-

BackOur board

Numis at a glance

Our Articles

28

Mar 2024

31

Jan 2024

Latest Transactions

London Stock Exchange Group PLC

£1.4bn

Co-global coordinator on the £1.4 billion sell-down of the London Stock Exchange Group PLC

March 2024

Custodian Property Income REIT

£237m

Sole financial adviser, sponsor and corporate broker

January 2024

Numis On Twitter

Debt Advisory Update

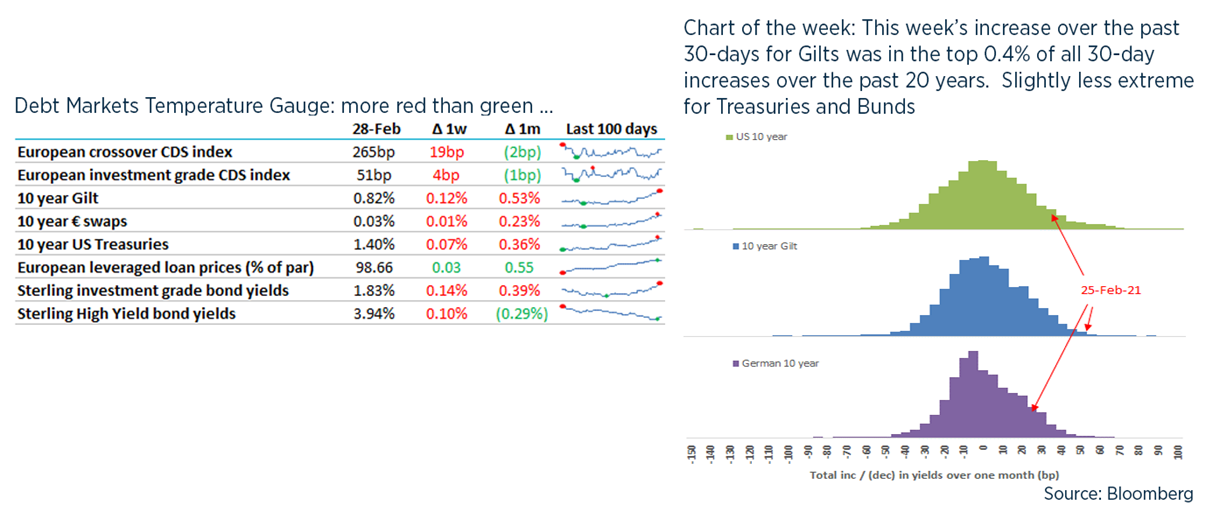

The best news this week was in the PM’s “roadmap” which is neither a map nor about roads: pubs can reopen on 12th April which makes today T-43, and counting.

TL / DR: rising government rates, costs of security, dealing with covenants

1. Rates of change

- As markets become sensitive to the risks of inflation, Government rates have jumped: Gilts have rarely ever risen more over 30 days than in this week, mainly January 2009 which you may remember being a busy time in the markets. But with rates so low, this 0.5% move is a 170% increase.

- There are better interest rate analysts out there than me e.g. this is a good article. While UK and European rates have risen in tandem with US Treasuries, US inflation is expected to be higher, as its stimulus is simply supersized. This means real rates have risen much more in the UK and Europe. Expect more action from ECB and a difficult speech by the Chancellor this week.

- Equity markets are not taking this particularly well but what of credit markets? So far so good:

- The Crossover index is a good measure of appetite – it’s risen in the past month but credit spreads are still as low as at the end of January.

- Some recent high yield issues are pricing below par e.g. Iceland’s recent bonds are at 97.5 – but this is all driven by underlying risk-free rates, with credit spreads unchanged.

- Leveraged loans are surging ahead – these have floating interest rates so should be unaffected by rising risk-free rates. Borrowers continue to cut margins on leveraged loans priced last year.

- We’re not seeing any changes in lending bank behaviour yet – they remain keen for good clients and will grudgingly rollover debt for more difficult stories. In fact, rising longer-term rates can be good for banks.

- I think it’s more likely that macro drivers will dominate: how quickly we all hit the shops in April and what happens to unemployment when the furlough finally ends. A weaker US$ could well cause more issues for exporters than an extra 0.5% on borrowing costs.

2. (in)Security

- We’ve had a few conversations with borrowers this week about loan security.

- Many institutional leveraged lenders need security as part of their pitch to their end investors (or ratings agencies for CLOs) that they will be safe in a downturn (as Ares says in this article – hope that worked for them this year.

- Banks can have more flexibility: security can achieve lower capital charges on loans but it is also a matter of whether credit teams are happy mixing with the hoi polloi as unsecured creditors.

- Typically a UK mid-cap might be asked to provide security or a debenture over all meaningful assets, which captures shares in subsidiaries as well as real assets, IP, debtors and bank accounts. For many companies, this is straightforward but can be onerous if assets are regularly bought and sold – in this case, maybe try compromising with just share pledges.

- Giving security to lenders makes it very difficult to introduce other creditors, not just for loans but also settlement limits, FX lines, bonding – no-one likes to be subordinated.

- The most important “unsecured creditor” to bear in mind is a DB pension fund deficit – in this situation, providing new security to lenders can be a problem all round.

- I would always recommend asking lenders how much more it might cost to go unsecured. I recently saw some useful research suggesting that on a like-for-like basis, investment grade companies would pay c. 0.20% p.a. more to be unsecured – in the past, I’ve had banks tell me 25-50bps impact on pricing, which for some might be a price worth paying and one that will probably be recouped in the next refinancing.

- Incidentally, this analysis might also be useful to anyone trying benchmark IFRS16 lease interest rates – get in touch if you’d like to discuss.

3. Covenants: the haves and the have nots

- Last week saw The Card Factory come out with another “Liquidity Update” (the third since Christmas).

- Based on our own conversations, we expect to see quite a few more of these over the coming weeks as corporates go through ‘going concern’ sign-off discussions with auditors.

- We are still seeing mainstream banks be constructive on covenants with any fees being pretty nominal, in line with last year’s Bank of England guidance.

- In contrast, Victoria plc’s third visit to the bond markets showed the benefits of planning for higher leverage, after it priced a new 5.5 year €500m deal at 3.625%.

- This marks the culmination of 3 years work by Victoria which has resulted in a genuinely bullet-proof balance sheet even despite its 3x leverage: loads of liquidity, no financial covenants and an acquisition war chest of €400m.

- As with Synthomer, more leverage and using the high yield markets has given Victoria significant freedom at <4% cost – the key is being big enough to get that BB / B public credit rating.

UK debt financings this week:

- LSL arranged a new £90m RCF with NatWest joining Santander and Barclays on a smaller facility.

- I should have mentioned this last week: Hostelworld signed a €30m loan with HPS to provide more liquidity: 9.25% which can be PIK with penny warrants over c. 3% of the company. I estimate all-in cost to be 13-16% depending on how the share price plays out.

- It’s a business day in London so of course TDR / Issas and EG are back in the market, this time for $1.8bn eq to fund its purchase of Asda’s petrol stations and OMV’s German Gas Stations. First-lien is guided at L+450bp and the second lien loan at E+700bp. Because Deloitte resigned as auditor, KPMG isn’t ready yet with the financials and so EG is having to privately-place £675m of bonds at 6.25% - which is about 1% premium for being illiquid.

- PureGym has also privately-placed €45m of high yield bonds for liquidity.

Our services

Numis is an ambitious, dynamic and innovative investment bank, driven to excel across all aspects of its delivery.