-

BackWhat we doNumis is an ambitious, dynamic and innovative investment bank, driven to excel across all aspects of its delivery.Investment Banking

-

BackLatest newsRead the latest news about our business, our people and our work, find out about our next events and conferences.News

-

BackWho we areOur collaborative environment and distinctive way of excelling , is nothing without our great people.

-

BackOur board

Numis at a glance

Our Articles

28

Mar 2024

31

Jan 2024

Latest Transactions

London Stock Exchange Group PLC

£1.4bn

Co-global coordinator on the £1.4 billion sell-down of the London Stock Exchange Group PLC

March 2024

Custodian Property Income REIT

£237m

Sole financial adviser, sponsor and corporate broker

January 2024

Numis On Twitter

Debt advisory update

OK, it’s a been a little while since our last “Three Things About Debt”. There’s been quite a lot on – and every time we sat down to write, there was a change in government policy, Chancellor or monarch. We won’t dwell much on the new king except that we enjoyed his greeting to Liz Truss this week: “Back again? Dear oh dear”. Here at least, he does speak for us all. In terms of money, the only change will be that Charles will face to the right on coins and notes whereas Elizabeth faced to the left; apparently it alternates for each monarch. Apart from Edward VIII who as ever tried to be different.

But the new king is old news: in a desperate bid to make us nostalgic for Boris Johnson’s competent and efficient government, Liz Truss has done more U-turns than when I tried to drive around Granada.

I’ve written a few drafts of this over the past couple of weeks but news just kept happening. This time I’m just going to get it out, safe in the knowledge that this government will generate something else for us to write about next.

1. What just happened and what does it mean for corporate financing?

- No matter how Truss / Karteng or their outriders tried to spin it, she was hoping for a better reaction to the first “Special Fiscal Operation”. It’s not so much the size of the uncosted or unfunded tax cuts but the attitude: “we’ll grow into this deficit”; this sounds very much like “you’ll grow into those trousers”, which is fine for my 13-year old son but less convincing if addressed to my 81-year old father.

- While Jeremy Hunt is not even as colourful as John Major (don’t forget Edwina Currie), he can probably sound more responsible and reassure the markets – getting some breathing time (I’m sending this before the Gilt market opens on Monday …).

- Anyway, there are better (or at least more eloquent) economists than me for you to read. I’ll just cover debt markets.

- Lending banks: for a while now, lending banks have been steadily getting more cautious, particularly depending on proximity of the borrower to consumer spending. Now it’s starting to get much more pronounced: we know of a few banks that are turning down any new clients in Consumer and Retail sectors while all credit teams are proactively seeking to understand better sensitivity of existing borrowers to rising rates and slowing demand. But banks have not stopped lending, providing the borrower’s case and creditworthiness stands up: a couple of acquisitions we are advising on are still moving forward, albeit at a slower rate and possibly with less leverage than before.

- Corporate bond markets: in the past six weeks, there have been just 2 sterling issues (Hiscox and Orsted). EUR markets have been better, with 36 deals worth €12bn pricing since 23 Sep, but this is down about 70% on prior years.

- Private placement bond markets: we know of a few deals that are yet to be announced, primarily for industrials. US investors are willing to put capital to work but they are not currently willing to provide these bonds in sterling, as cross-currency swap markets into sterling are too volatile. And UK investors are more focused on picking off choice assets in the sterling bond markets.

- Leveraged finance: September was supposed to see the restart of activity after a depressing summer but none of the deals which have come in Europe and the US have gone completely according to plan.

- I had at first thought that Flutter’s $1.2bn bn of term loans had been a success, pricing at SOFR+325 at a price of 97c / $ (a yield of about SOFR +400bp ~ 7.5%). But then I noticed that Barclays had abandoned plans to syndicate a further €500m of debt and instead had cooked up a $750m “Term Loan A” to be held by it and other banks.

- White & Case has a good primer on the rebirth of “Term Loan A” – safe to say, it has not been Plan A for many years for large amounts of debt to be retained by underwriting banks: putting lipstick on it and calling it Term Loan A does not make the pig any prettier.

- Generally, the last few months have been a disaster for underwriting banks: Citrix in the US was the most high-profile where banks lost $700m on the portion of the debt they placed into the market – with an equal size again being retained for syndication in better market conditions (good luck with that!). And even then, the equity sponsor Elliott Associates took down $1bn of this at 84c / $: this is literally the banks giving Elliott $160m.

- Private debt funds: these remain the best-funded source of long-term debt and have backed most of the UK public-to-private deals of the last year. But they are busy, jammed with new deals and being selective. And their rates are going up. Some of the funds have stopped lending altogether, worried about credit problems in their portfolios. But the main problem is their cost: at SONIA +700bp, this could mean interest costs of >12% next year, which makes the LBO maths challenging. The only way to address this is to reduce the quantum of debt, reducing total interest costs, and which will also reduce leverage (which should reduce the percentage rate being charged).

- It is also possible that pension funds may reduce their allocations to private credit substantially over the next few years (more on this another time).

2. Interest rates & hedging

- How do you know if someone fixed their mortgage costs earlier this year? Don’t worry, they’ll tell you.

- And similarly for corporates: the average UK mid-market corporate has little interest rate hedging in place, often because they are reliant on bank funding.

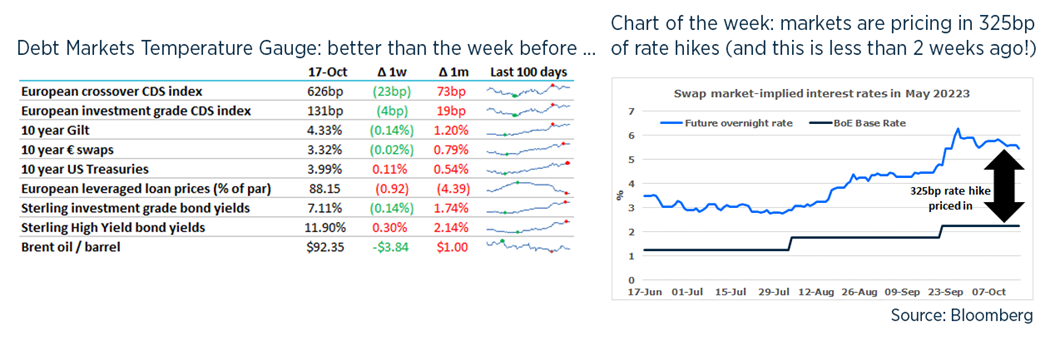

- The interest rate (swap) market is currently pricing sterling overnight rates (≈ BoE Base Rate) at 5.5% in May 2023, falling to below 5% in 2025. If you really want to fix your interest costs then swap rates are around 5% (which is why mortgages are now approaching 6%).

- If you really do want to (or have to) hedge interest costs at current levels then the simplest way is to buy a cap from a bank: banks can sell these with simple documentation and no need to consider credit quality.

- The bad news is that current levels and volatility make caps expensive: a 3-year cap on SONIA at 5% will cost 3% of the notional i.e. to hedge £100m would cost £3m.

- While some REITs have spent significant amounts buying caps (e.g. Warehouse REIT spending £10m to hedge £100m (more details here), most of our conversations with clients are about interest rate swaps: where a corporate ‘swaps’ the cash flows on a notional amount with a bank, with the corporate paying a pre-determined fixed rate and the bank paying whatever UK overnight rates turn out to be (the ‘floating’ leg). The bank can use the floating payment to meet its floating rate loan interest.

- The key difference between buying an option and entering a swap is that the swap contains credit risk. This is no longer esoteric financing knowledge now that the pension funds and their derivatives are headline news.

- If a corporate agrees to pay say 5% and for some reason rates fail to rise as expected then this has become an onerous contract: the corporate is still required to pay the higher payment even though market rates are much lower. So the bank has to be worried about whether the corporate will be able and willing to keep paying in the scenario when rates stay low: this is a contingent credit risk.

- This is unlike a cap, where if rates stay low then the corporate’s option just expires.

- So to put on an interest rate swap, the bank needs to protect its credit position: it will want to be equal-ranking with the rest of the debt, and some banks may want to share security and upstream guarantees from key group companies. They will also need to negotiate an ISDA which can take weeks.

- The bank also needs to charge for this contingent credit risk (called a Credit Valuation Adjustment). There are there more complicated charges they will add, to cover funding and capital costs. Credit charges on swaps can really depend on the market, the specifics of the deal and what other trades the two counterparties already have between then. A 3-year interest rate swap might historically involved a charge of 0.05-0.15% p.a., added onto the fixed rate.

- But in current markets, the risk of corporates facing an out-of-the money swap and then defaulting is much higher than a month ago:

- Volatility: interest rate volatility is much higher so the chance of rates ultimately staying lower than expected is higher.

- Levels: at 5%, banks perceive it to be more likely that rates might be 200-300bp below expectations than it was when rates were about 0.25%.

- Credit: the average credit quality of corporates is also lower.

- So even if you to pay today’s rates, putting on a hedge in this environment is not a walk in the park.

- In passing, these credit complications and charges were why the pension funds agreed to provide collateral to their counterparties. Turns out turning credit risk into liquidity risk didn’t work out that well.

3. Twitter

- To finish on a lighter note, Musk’s abrupt letter to Twitter means that his banks will need to fund the Twitter debt financing – I wonder if he texted Morgan Stanley to let them know in advance.

- In normal times, they would be approaching the leveraged finance market before the deal had closed but they don’t have enough time to do this before 28 October – I don’t think they’ll even be out this year.

- At some point though they will want to derisk themselves but it seems unlikely that they will be able to sell the debt to investors without losing money.

- The banks promised Musk the most risky tranche would cost no more than 11.75%, which seemed fine back in April when comparable debt yielded 9.5%. But now CCC debt yields almost 16%, this means the banks will lose $400m on this tranche alone.

- It will be fun to see if Elon is part of the management presentation to investors: “come buy this debt for a business that I really didn’t want to own because its numbers are made up and full of bots”.

- I joined Barclays in September 2007 when there were many stuck underwrites on the books: INEOS, Boots, AA Saga to name a few. It wasn’t until 2013 that the AA Saga debt was refinanced and Acromas finally exited the portfolio, overstaying its welcome like our last four prime ministers.

Selected Interesting recent UK financings

- Molten agreed a £!50m NAV loan with JP Morgan and Investec, at SONIA +550bp.

- Grafton signed a £334.5m ESG-linked RCF (carbon emissions, workforce diversity and community support targets).

- Vue and Cineworld announced debt restructurings. Vue’s appears to be a more clinical approach, with its lenders taking ownership and control, while Cineworld is heading for a more messy Chapter 11 process.

- Johnson Service Group agreed a £85m 3-year RCF.

- TfL agreed a £200m RCF from a group of banks including NatWest and Bayen LB.

- Castore agreed a £50m 3-year RCF with HSBC, BNP Paribas and Silicon Valley Bank.

- AB Foods increased its RCF from £1.1bn to £1.5bn, with a 5+1+1, with no financial covenants (the benefits of being A-rated).

- Ricardo signed a £150m 4-year RCF at SONIA +165-245bp.

- Schneider lined up a £4.1bn bridge to buy the minority shareholders in Aveva. I think up-front fees were 5bp.

- ECP’s buyout of Biffa was funded with just £175m of acquisition debt (and over £1bn of equity) while the USPP’s were incentivised to remain in place – meaning the structure must remain formally investment grade.

- Hyve agreed a £115m refinancing with HPS, alongside £20m of super senior RCF from HSBC. HPS’s debt costs SONIA +775bp while HSBC’s loan is SONIA +350bp.

- Finally, probably the first of many: Wetherspoon’s has received a covenant amendment out to July 2023.

Disclaimer

This briefing has been prepared using publicly available information and should not be relied upon for any investment decision. Numis does not make any representation or warranty, either express or implied, as to the accuracy, completeness or reliability of the information contained in this briefing. Numis, its affiliates, directors, employees and/or agents expressly disclaim any and all liability relating to or resulting from the use of all or any part of this briefing or any of the information contained herein. This briefing does not purport to be all-inclusive or to contain all of the information that recipients may require. The information contained herein is subject to change and Numis accepts no responsibility for updating it.

Our services

Numis is an ambitious, dynamic and innovative investment bank, driven to excel across all aspects of its delivery.