-

BackWhat we doNumis is an ambitious, dynamic and innovative investment bank, driven to excel across all aspects of its delivery.Investment Banking

-

BackLatest newsRead the latest news about our business, our people and our work, find out about our next events and conferences.News

-

BackWho we areOur collaborative environment and distinctive way of excelling , is nothing without our great people.

-

BackOur board

Numis at a glance

Our Articles

28

Mar 2024

31

Jan 2024

Latest Transactions

London Stock Exchange Group PLC

£1.4bn

Co-global coordinator on the £1.4 billion sell-down of the London Stock Exchange Group PLC

March 2024

Custodian Property Income REIT

£237m

Sole financial adviser, sponsor and corporate broker

January 2024

Numis On Twitter

Debt Advisory Weekly

Since the referendum, there seemed to be only two realistic outcomes: no deal or no Brexit; any middle ground is either pointless or unacceptable to Brexiteers / the EU. As with all major European decisions, this difficult choice has been put off for as long as possible but maybe now the time is here.

TL / DR: Zombies and vultures; Putting a price on relationships; Tally sticks

1. Won’t someone please think of the vulture funds?

- Back in 2010, many companies became ‘zombies’: still superficially serving equity but really run for the benefit of their reluctant creditors. It wouldn’t be fair to name too many but for example it took many years of repositioning and a rebrand for Enterprise Inns to rise again (my son knows a different approach to curing zombies).

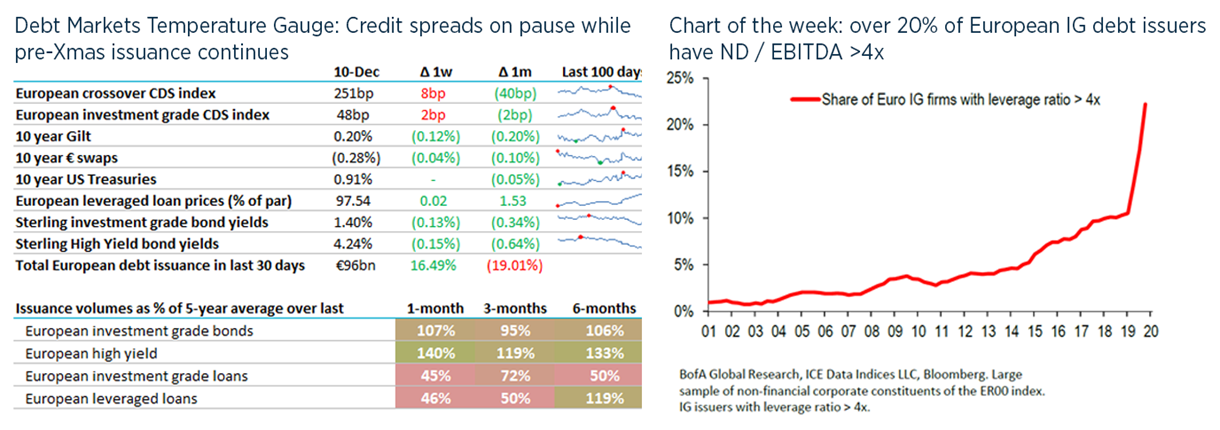

- Even if business models remain intact post-COVID, leverage for some will remain persistently high due to this year’s debt and weaker economic growth – as shown in this week’s chart.

- Listed companies and their investors have long viewed “normal leverage” to be 1-2x leverage against a covenant of 3x, even as the debt servicing costs fell from nearly 6% to nearly zero

- As a parallel, in the same time period we all became more comfortable justifying higher house prices on the basis that mortgages had never been more affordable.

- Are we about to see a shift to accepting 3-4x as normal? After all, debt is rarely repaid but is normally refinanced into new debt so if higher leverage is accepted then it becomes sustainable, particularly at these low rates.

- Alongside this, this week there was a further extension of Government protection for management against winding up and wrongful trading.

- Ironically, distressed debt businesses are suffering: CVC has closed its European distressed debt fund, with 15 redundancies.

{kind=link}

2. How much is a good relationship worth?

- It seems right as Christmas approaches that we should praise the importance of relationships as only bankers can: by putting a price on them.

- On a couple of recent deals, we have helped clients weigh the intangible value of a reciprocal and long-term relationship against the tangible cost of higher debt costs.

- At the end of well-organised debt process designed to maximise competition, not everything can be quantified into a grid or term sheet: sometimes borrowers need something from lenders without it being “a transaction” e.g. extra-quick responses or to bend internal processes to fix a short-term problem.

- Our Debt Advisory team includes ex-lending bankers and borrowers, so we have real-world experience of how a good debt relationship can really help.

- In recent weeks, our clients have sometimes chosen proposals that cost a little more but with more flexibility that might be important in the future. In one of those cases, we were then able to use competition to get that flexibility for free, but in the other our client decided to pay more for the relationship – never an easy decision.

- While all additional cost hits shareholders’ return, it is rare that a business plan can be broken by 25-50bp of additional debt cost (which is less than Libor has fallen this year). And bear in mind that the average Excel spreadsheet has errors in 1-2% of cells.

3. The Rate of Return

- Nearly everything in finance is about ‘rates of return’ but like me you’ve probably been kept awake at night wondering “return of what to whom?”.

- We can help you sleep more easily: 800 years ago, English Kings used to keep track of what taxes had been collected and handed over to the Exchequer using tally sticks: each stick was notched and then halved down the middle, with the tax collector keeping one half (“the stock”) and the exchequer keeping the other. There are some nice pictures of sticks here.

- When it was time for the tax collector to be audited, he presented his half-tally which was matched against the retained half; this enabled the tax collector’s liability to be discharged and the sticks destroyed.

- Financial innovation has been with us forever: after about 200 years, as tax revenues slowed, King Edward III bought goods from merchants with an IOU who would then take their claims to the exchequer and receive a half-tally in exchange, which could in due course be given to the local tax collector instead of paying taxes in cash (coin). Now tallies were issued in advance of taxes being paid – and the tallies would be “returned” to the Exchequer by the tax collector.

- These “redeemable stocks” were issued at a discount e.g. a tally for £100 of future tax liabilities might be issued in return for an IOU of £80 – a 25% “rate of return” (hence also “tax return”).

This was also the origin of the repo market as the stocks could also be used as high-quality collateral for merchants to raise their own debt privately. - Government debt as prepayment of taxes ties into Modern Monetary Theory (much more from the Bank of England here) and the ability of a sovereign country to print money via QE.

- The “independent” governor of the Bank of England was unusually candid in a Sky News interview in June when he confirmed that the Bank of England had financed government spending in March by buying new Gilts when the market was unwilling.

UK debt financings this week:

- Bytes announced its inaugural £50m RCF as part of its £350m IPO *** Numis Advised ***.

- Metropolitan Thames Valley Housing signed a £50m 3-year sustainability linked RCF with BNPP.

- Kinectic Capital provided a £39m loan to Jensco to finance the development for student housing.

- InterContinental Hotels Group secured a waiver until Dec-21 and had covenants relaxed through 2022; with max leverage now 7.5x.

- Jaguar Land Rover issued 7NC3 $650m high yield at 5.875%, upsized from $500m and well inside its guidance of “low 6%s”.

- ContourGlobal (UK-listed international power generation) issued €710m of 6 and 8-year HY at 2.75% and 3.125% - about 0.5%pt inside guidance.

Our services

Numis is an ambitious, dynamic and innovative investment bank, driven to excel across all aspects of its delivery.