-

BackWhat we doNumis is an ambitious, dynamic and innovative investment bank, driven to excel across all aspects of its delivery.Investment Banking

-

BackLatest newsRead the latest news about our business, our people and our work, find out about our next events and conferences.News

-

BackWho we areOur collaborative environment and distinctive way of excelling , is nothing without our great people.

-

BackOur board

Numis at a glance

Our Articles

28

Mar 2024

31

Jan 2024

Latest Transactions

London Stock Exchange Group PLC

£1.4bn

Co-global coordinator on the £1.4 billion sell-down of the London Stock Exchange Group PLC

March 2024

Custodian Property Income REIT

£237m

Sole financial adviser, sponsor and corporate broker

January 2024

Numis On Twitter

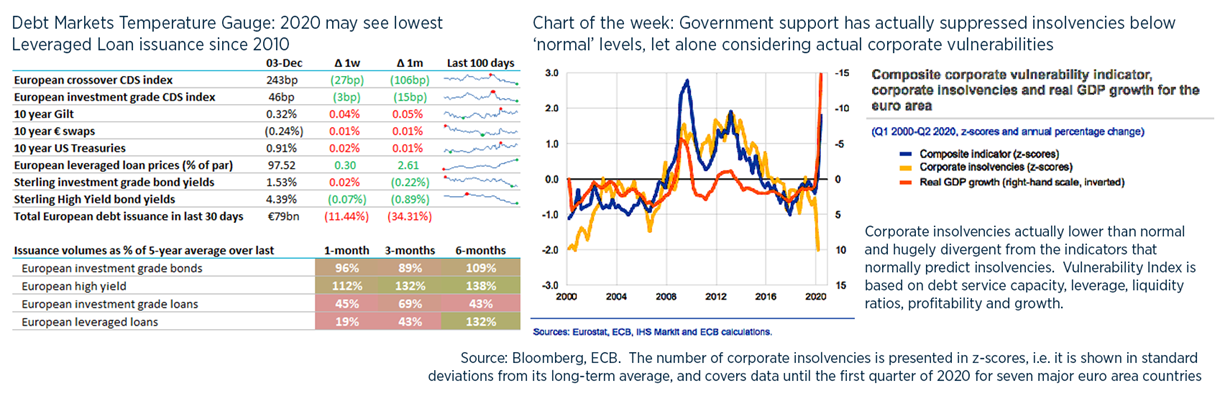

Debt Advisory Update

We hope you enjoy your scotch eggs at the pub this evening.

TL / DR: convertibles get an outing, pension deficits and gutting debt protections

1. Convertibles get an outing

- According to investment bank convertible bond teams, it is always the right time to issue a convertible bond.

- if stock prices are high then the conversion price will be 30-40% up and probably at an all-time high.

- if prices are low because business is tough then the convert may be one of the few debt capital markets open to you.

- From an issuers’ perspective, the problem with converts is that they are debt when you want them to be equity, and equity when you want them to be debt. But your choices are always constrained when you sell optionality.

- A few recent UK deals highlight that they can really be flexible tools in the right situations:

- IWG sold £350m 7-year convert at 0.5% coupon and 40% premium. This was upsized from £300m and priced at the low end of coupon and high end of premium. Embedded credit spread was 350bp and implied vol of 30%. This will fund an acquisition war chest.

- Capital & Counties sold £275m of 6-year exchangeable bond (into part of its Shaftesbury shareholding) at 2% coupon.

- Both of these achieved long-dated debt without significant covenants and a discounted coupon, based on giving up some upside if share prices rise significantly.

- Minimum size remains a constraining factor for many of our clients: markets are generally interested in deals of at least £80m. There have been only 10 sterling convertible bonds for £100m or less in the past 10 years.

- Finally if you ever do a convertible bond then it’s obligatory to name the project after an E-Type, etc.

2. Et in Arcadia, ego

- This week’s news on Arcadia and Debenhams prompted me to reflect on pensions and how to measure a liability today which can extend decades into the future.

- I took a look at the accounts of BHS and Arcadia back in the 2000s when it paid the famous £1.2bn dividend to Tina: at the time, the schemes were in surplus – but this was with future pension payments discounted at almost 7% one year.

- Back in 2007, 10-year gilts yielded 5.5% and in 2008 AA sterling yields exceeded 8%!

- For any 40-year stream of cashflows, moving the discount rate from 7% to 1% increases the present value by 140% (because of convexity). If a scheme is fully funded at a 7% discount rate then it will have a deficit of 1.5x assets if discount rates fall to 1%.

- My takeaway is not that Arcadia was fine in 2006 but in leveraging itself up with the special dividend, it should also have hedged itself better against falling rates either by specific interest rate hedges or by switching to bonds as did Boots did in 2001 (also providing John Ralfe with a career in pension commentary).

3. Disenfranchising leveraged lenders

- Cov-lite comprises over 80% of broadly syndicated market and lending standards have continued to loosen with Moody’s recently assessing recent loans as about as bad for lenders (good for borrowers) as ever.

- Not surprisingly, recent data suggests cov-lite loans result in lower recoveries for lenders in the event of default: S&P estimates median recoveries for cov-lite are 34% lower than for covenanted deals (despite covenants really only being included for the deals which are worse / harder to sell).

- A new development was reached this week with Blackstone managing to sell bonds in Ancestry.com where lenders’ voting rights are no longer proportionate to their holdings. Instead, any individual bondholder’s votes are capped at 20% unless Ancestry.com wishes otherwise.

- A representative from the European Leveraged Finance Association called it “just awful”, but perhaps the finger should be pointed at investors that provided $9bn of orders for the deal.

Soon leveraged debt will be reclassified as low-yielding preference shares with minimal governance rights. - In the same week, the lowest yielding “high yield” bond of the year was issued in Japan: 1% for Aiful. Again, no-one is forcing investors to buy this…

UK debt financings this week:

- Volution has signed a 3+1+1 year £150m RCF with the margin linked to sustainability performance targets.

- LMAX Group has agreed a 4 year £40m RCF with SVB.

Our services

Numis is an ambitious, dynamic and innovative investment bank, driven to excel across all aspects of its delivery.